| 2017 | 2018 | ||||||

| Price: | 98.25 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 35 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 3,400 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -422 | EBIT | 0 | 0 | |||

| TEV (in $M): | 3,000 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- ELLIE MAE INC ELLI S 03/16/2018

- ELLIE MAE INC ELLI 05/18/2014

- ELLIE MAE INC ELLI S 05/01/2014

- PULTEGROUP INC PHM S 06/28/2021

- TREZ CAPITAL SR MTG INVST CP TZS. 08/23/2018

- BLEND LABS INC BLND 12/28/2023

- CAPITAL ONE FINANCIAL CORP COF 03/28/2018

- CROSSROADS SYSTEMS INC CRSS 11/20/2020

- PROVIDENT BANCORP INC PVBC 11/16/2019

- MANHATTAN BRIDGE CAPITAL INC LOAN 09/26/2023

Description

Ellie Mae, Inc. (ELLI)

Investment Thesis:

ELLI is an attractive long-term investment in a quality business, which makes software that helps to streamline and automate the mortgage origination process. ELLI’s Encompass software is quickly becoming the standard for the mortgage origination industry and has compounded revenue at a 45% CAGR in the last 5 years. We think it will continue to compound revenue at 25+% and 22+% CAGR for the next 3 years and 5 years, respectively. It will have $5 and $8 in earnings per share exiting 2019 and 2021, respectively. The revenue growth is driven by the market share gain, price increases, growth into new verticals and higher technology spend by their customers on mortgage originations to save cost and comply with new regulations. Short interest is 10% of the float and the company’s shareholder base has been overly concerned with a likely drop in mortgage refi activity in 2017 vs 2016. These holders have been concerned that the company will have a difficult time meeting 2017 consensus expectations. This was the case last year as well, but the Company consistently beat consensus expectations for the last two years in each quarter. Given the strong refi years in 2015 and 2016, we have already been modeling weaker refi activity. Furthermore, The Company is less exposed to refi activity than people think. ELLI currently has no exposure to the top five banks. These banks have relatively higher share of the refi market. Moreover, since it is much easier to close a refi loan vs a new purchase, banks tend to need to buy more seats from ELLI as their business mix shifts towards purchases. We believe people also think that the guidance has increased risk given a couple of regulatory tailwinds are going away, and because big banks are expanding back into the purchase market. Again, we had already factored these risks into our model and still have substantial differentiation compared to the Street. We actually think there is less risk to beating Street estimates following the conservative guide for 2017. ELLI recently revised its customer contracts to include a base fee increase of $5 per annum. Base fee per month per seat for new customers has already gone up from $75 last year and will be $85 this year. Based on our conversations with sell side and other investors, most haven’t realized the current higher base fees and the changes in the contracts. To give you an idea, current average price per seat per month was $68 and it will be $95 exiting 2019 based on the math we just described, which is a 40% price increase on their contractual revenue just from these contract changes in less than 3 years. This also means that they need to rely less on mortgage origination volume, a major concern for the investors currently as interest rates goes up. In addition, ELLI has launched a new vertical (i.e. construction loans), which can eventually do 5 to 7% of the current loans. Easing of credit lending standards could drive the growth in nonqualified mortgages and could be another tailwind for ELLI. Also, last year ELLI added a record number of seats, a lot of which will become productive this year driving up number of active seats and adding to the revenue. There are plenty of new regulations/compliance requirements on the state level which will keep the tailwinds behind ELLI’s software adoption (please see appendix). The lenders also need ELLI for cost savings and to serve borrowers competitively using the latest technology. We also think the refinance market will bottom out this year and rising rates will be less of a concern going forward. Industry originations are now running 1% higher for the year and 4% for the next quarter than when the management gave its last guidance. Operating leverage should be much better throughout the rest of the year and going forward, which is underestimated by the street. ELLI’s business is highly scalable given the SaaS model. Only about 7% of cost-of-goods is variable. It is mostly done with heavy upfront investments in its Generation 2 product, and should see meaningfully higher margins than consensus in the near and long term. We think that ELLI will reach its long-term target margins of 35% to 40% EBITDA exiting this year and will eventually break into the high 40s by 2021 or management will use incremental dollars to enter new verticals, which is not included in our base case. We won’t be surprised if management increases the long-term margin guidance at the analyst day on March 7th. By 2021, we think the company can earn over $8 in EPS. A relatively conservative 25x multiple for a highly predictable, sticky (90% recurring & 70% contractual fee based) and growing business like this results in a target of over $200, which is a 21% IRR in 3.8 years. This is not even factoring in optionality for the company to enter new verticals like auto loans or servicing, or even winning a deal with a top 5 bank.

Thesis details

-

ELLI will continue to beat on growth expectations: ELLI is a compounder benefiting from the secular growth. We think ELLI can grow its revenue at a 26% CAGR for the next 3 years and 22% for the next 5 years through:

-

Contractual fee increase: ELLI recently revised its customer contracts to include a base fee increase of $5 per annum, and changed the contract length from 3 to 5 years making it more sticky. Base fee per month per seat for new customers has already gone up from $75 last year and will be $85 this year. Based on our conversations with the sell side and other investors, most of them haven’t realized the current higher base fees and the changes in the contracts. The current average length of contract is somewhere between 3-4 years, so ~1/4 of contracts are getting renewed each year. In addition, there are still a lot of customers with grandfathered contracts which are at a significantly lower price. All of these customers will renew at a higher rate soon as ELLI makes no concession for the base fees no matter how big is the customer. To give you an idea, current average price per seat per month is $68 and it will be $95 exiting 2019 based on the math I just described, which is a 40% increase just from these contract changes in less than 3 years. This also means that they need to rely less on mortgage origination volume, a major concern for the investors currently as interest rates goes up. By the way, don’t expect management to be very forthcoming about this in public. They are likely sensitive to client perceptions. The way ELLI management describes the price increase is based on incremental value that comes from R&D. In fact, customers are actually committing to price increases irrespective of any incremental value that ELLI gives.

-

Seat growth from higher industry penetration: Currently, ELLI has 215k contracted seats and is 25% penetrated among the lenders and brokers (850k industry seats) excluding mega lenders (200k seats). About 30% of national mortgages are originated through the ELLI platform. The recent government disclosures suggest that the TAM is higher than originally thought by the company as not only front end originators, but also back end mortgage employees are using its platform. Especially because lenders need more seats for a purchase loan vs. a refi loan. As the market shifts to purchase loans, ELLI has benefited from growth. ELLI is considered the best mortgage origination software. Over the years, it has taken enormous share from Calyx and Cadence (Accenture) and is quickly becoming the de facto standard for the industry. Like most software businesses, this should be winner-take-all. Since ELLI has the most scale, it should invest the most in R&D and have the best products which should give it even more market share. Customer choice for the software mostly comes down to its own internally developed tools or ELLI’s Encompass software. The S curve below shows that ELLI is still early in the adoption of its revenue.

Source: Ellie Mae

-

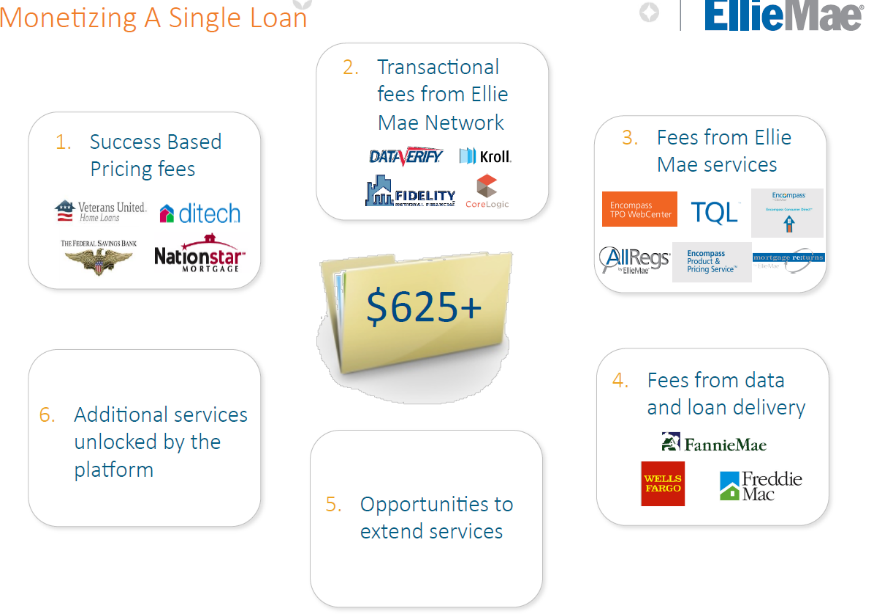

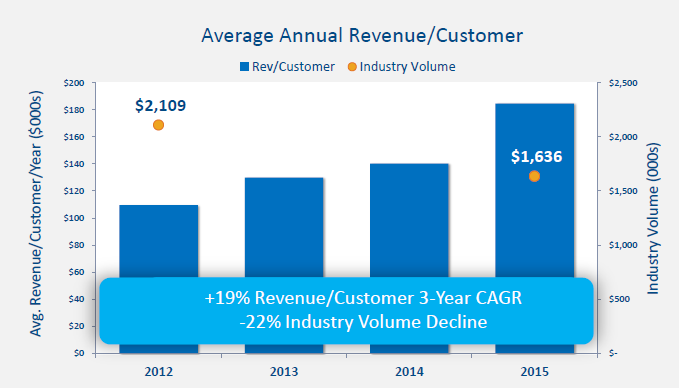

Higher revenue per seat through cross-sell: ELLI is only making about $145 per loan origination as of today. If customers adopt all of the current ELLI products, ELLI can generate $400 per loan. Our checks indicate that several new regulatory and compliance requirements are pushing customers to increasingly rely on ELLI’s full product offering, which will continue to be a tailwind for the next 3 years (see appendix). The company is also working on new products and aims to acquire 1 or 2 add-ons per year. There is about $625 per loan spent today on technology and we see no reason why all this spend can't go to ELLI over time as it becomes the status quo of the industry. An average loan costs about $7,000 to originate today. Independent studies show big ROI on implementing ELLI’s software. ELLI has significant room to cross sell added functionalities. By utilizing ELLI’s suite of bundled products and services, customers avoid the risk and effort of cobbling together two or more solutions from competing vendors. To the extent users do not subscribe to the bundle, ELLI could sell more of the Encompass services such as document preparation, EDM, compliance services, product and pricing services, fraud services, income tax verification services, flood services, appraisal services, website hosting and customer relationship management. Current offerings such as Allreg are only being used by 20% of the customer base and can be adopted by 2/3 of the users. Allreg can add somewhere between $25-50 per user per month. In the last three years revenue per customer has gone up 2.8x with 19% revenue/customer CAGR, while Industry volume has declined -22%. Just maximizing users expands ELLI’s revenue to $1 billion, and maximizing adoption across all potential users expands revenues to $6.25bl. We are only assuming ~2.2 revenue per customer growth by 2021 from 2015, which yields about $950mm in revenue by 2021. If ELLI gets all the spend described in the chart below then there could be significant upside to our estimates.

How ELLI can maximize revenue per originated loan

Source: Ellie Mae

-

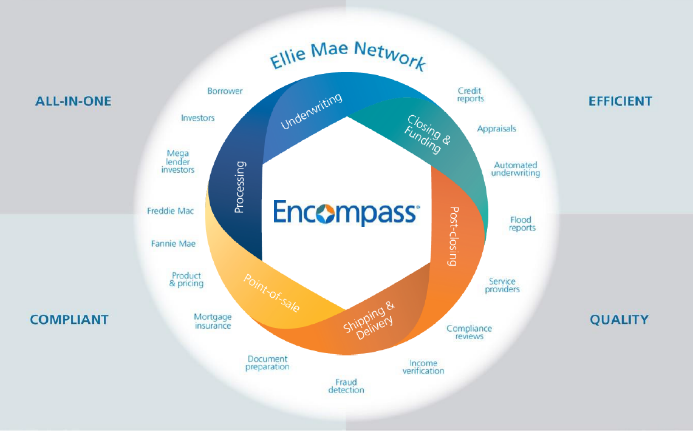

Expanding the use of the Ellie Mae Network: The network provides mortgage originators electronic access to many of the investors and mega lenders, and most of the service providers, that they need to interact with in order to process and fund loans. These transactions include electronic ordering of credit reports, appraisal services, title and flood reports and accessing the automatic underwriting systems of Fannie Mae and Freddie Mac. ELLI continues to encourage providers of settlement services to deliver these services electronically through the Ellie Mae Network. ELLI will continue to add functionality and services to the Ellie Mae Network so investors, lenders, and service providers can do business more effectively with mortgage originators using Encompass. ELLI introduced the TQL program in 2011 and continues to work to add more of its lender and investor customers to this program. Investors and lenders can populate mortgage originators’ Encompass software with specific compliance, underwriting, and documentation requirements for loans prior to delivery in order to screen loans for quality and regulatory compliance. Network revenue is only about 10% of the total revenue. 13 different transaction capabilities are built in the network, but clients are using only 7 on average. Higher end services such as Title service ($7 per transaction), Appraisal ($10), IRS automation ($16) and Special Loan File ($25) are only 2-3% penetrated, whereas most of the network revenue is currently coming from credit report, which only costs about a dollar.

-

Market share gain from higher purchase mix: The top 5 lenders have been scaling back from the mortgage market because they find the loan category less profitable (share of the top five banks went from 52% in 2012 to 35% in 2015). Higher purchase mortgage volumes vs. refinancing also help local banks gain share because of their relationships with customers. As a result, ELLI’s customer base is gaining share since it is more weighted towards purchase mortgage. Also, purchase loans need more officers than refi, so ELLI’s existing customers have been buying more seats. The refi mix is supposed to decline to almost ~25% by 2018 from 48% in 2016. In 2012, refi was as high as 70%, and the average post Great Recession has been close to 60%. The mega lenders have 200k seats and still control a big portion of the origination market. We think ELLI could land a deal with one of the top lenders anytime in the next two years. Top lenders have been facing cost pressures and their internal software seems to be clumsy and outdated. ELLI has been increasingly bullish regarding signing a top tier bank.

-

Growth from new construction loan vertical and nonqualified mortgages (non-QMs): ELLI just launched a new construction loan vertical this year. It estimates the size of the opportunity at 5-7% of its current loans. We think it will offset some of the refi drop. If the Trump administration eases regulations for the financial industry, non-QMs might pick up again with easing credit standards, and it could be a tail wind for ELLI. Right now, banks have no idea about the penalties, the capital requirements and the regulatory risk involving non-QM, which has kept them in the back seat.

-

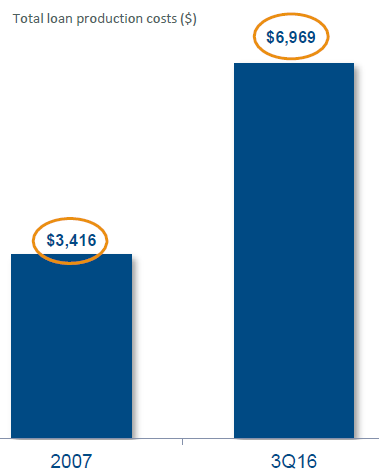

Regulations and greater focus by customers and regulators on data security and consumer privacy driving Encompass adoption: New mortgage regulatory and compliance requirements (See appendix) are causing lenders to adopt ELLI’s software at a rapid pace to avoid cost and errors. The Mortgage Bankers Association (MBA) estimates that it costs around $7,000 to originate a loan, which has doubled in five years. A third-party study from MarketWise Advisors shows that ELLI’s Encompass can benefit a lender as much as $970 per loan and a client $572 per loan. A client’s savings generally increases with the adoption of additional services. Recent high-profile data security incidents affecting banking institutions and cloud-service software providers have resulted in an increased focus on data security by ELLI’s customers and ELLI’s customers’ regulators. We expect the industry focus on data security to continue to increase as companies generate greater amounts of data and as future data security incidents occur. The chart below shoes the trend in loan production cost.

Source: Mortgage Bankers Association performance report

-

Customers Adopting Multi-Channel Strategies: Customers are developing multi-channel strategies beyond a single retail, correspondent or wholesale mortgage lending channel in order to grow their businesses. The requirements of these different channels vary and in order to maintain a single operating system, customers must use a robust system with customizable functionality driving the adoption for ELLI products.

-

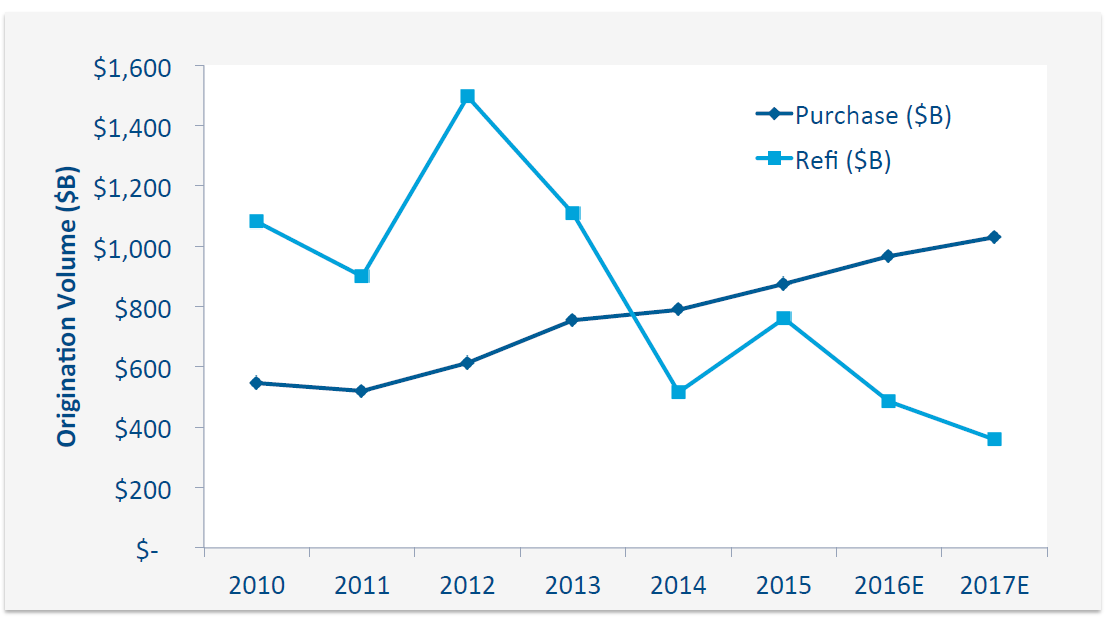

Increasing purchase volume: There is significant pent up demand from growing household formations. There are about 87M Millennials which would affect the growth of purchasing volume in the future. The chart below shows the improving trends in purchase volume, which are less sensitive to interest rate. Currently agencies forecasts suggest a 6% growth this year and a 7.5% growth next year.

Source: Ellie Mae

|

|

|

Source: Ellie Mae

-

Sticky recurring SAAS business with pricing power and high revenue visibility

-

Our checks with customers indicate high switching costs and high customer satisfaction, which gives ELLI strong pricing power in the longer term. Encompass software delivers efficiency, reliability and cost-savings in this highly regulated market with constant need of higher compliance. The low fixed fee and variable fee structure keeps the attrition low. It has retention in the high 90s. Rarely does a client leave and go to a competitor even during times of low mortgage volumes. In 2014, when mortgage volumes went down 40%, it only saw 5.5% attrition in seats, where 67% of the attrition was from reduction of seats/going out of business and the rest from consolidation in the industry.

-

ELLI has significant pricing power because of its sticky product. It raised prices from $75 last year to $85 per seat per month this year for new users. Now it has $5 annual price increase built into the new contracts. About one fourth of the clients are renewing each year and this increase is not factored correctly into the street numbers as we described earlier.

-

As ELLI grows its network a strong network effect will make its product even stickier. We think with the Generation 2 platform, ELLI will gain more share and widen its moat. Its next-generation platform leverages a new open secure and scalable architecture so that lenders and partners across the network can work more efficiently and seamlessly. In addition to releasing new updates to Encompass, ELLI has also launched new Encompass Connect solution suite, which helps improve visibility and collaboration between loan officers, third-party originators, developers and homebuyers this year. It also released Loan Officer Connect this year so that loan officers can originate and move loans forward quickly while gaining instantaneous and secure access to Encompass from any device. This comes on top of TPO Connect, third-party originator connects, which provides wholesale and correspondent lenders an easy and collaborative platform to do business with their third-party partners. At the end of the first quarter, ELLI will be releasing Consumer Connect and Developer Connect. Encompass Consumer Connect enables lenders to deliver a state-of-the art, engaging, self-service online origination experience for homebuyers, and one that lenders completely control and easily create. Encompass Developer Connect provides developers with APIs, tools and a comprehensive developer portal. Developers will be able to create new features for Encompass, easily integrate Encompass with external systems and data, and build and deploy custom applications in the cloud. This will generate greater value across the network, and increase the stickiness of the Encompass lending platform. Later this year, ELLI will introduce the first release of Encompass NG, focused on mid-market customers and then progressing to subsequent releases as we move into 2018, to address both strategic and enterprise customers. By creating an open lending platform, ELLI can accelerate its growth. In addition, lenders realized that they needed to adopt technology not only to overcome cost and complexity, but to become more responsive and competitive for their customers.

-

Margin leverage

-

ELLI is done with most of the heavy investments for its Gen 2 platform. The street is under estimating the operating leverage. Only 7% of COGS is variable and rest should grow at 10-15% per annum according to the company. Its current marketing team is fully grown and capable of handling the big clients and rest of the market. Beat on margins will widen after Q1, and it should reach its target margin i.e. 35-40% EBITDA in 2017. We think longer term EBITDA margins will be in high 40s. We are expecting that ELLI will increase these margin targets on the analyst day on March 7th. Note that ELLI has already done the majority of the heavy investment in the sales, support and compliance staff in order to go after big lenders.

-

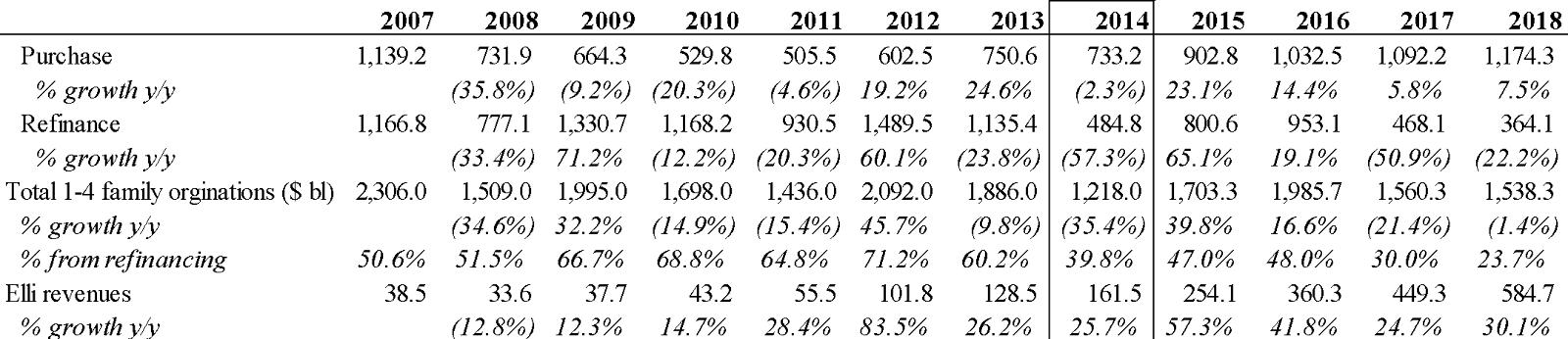

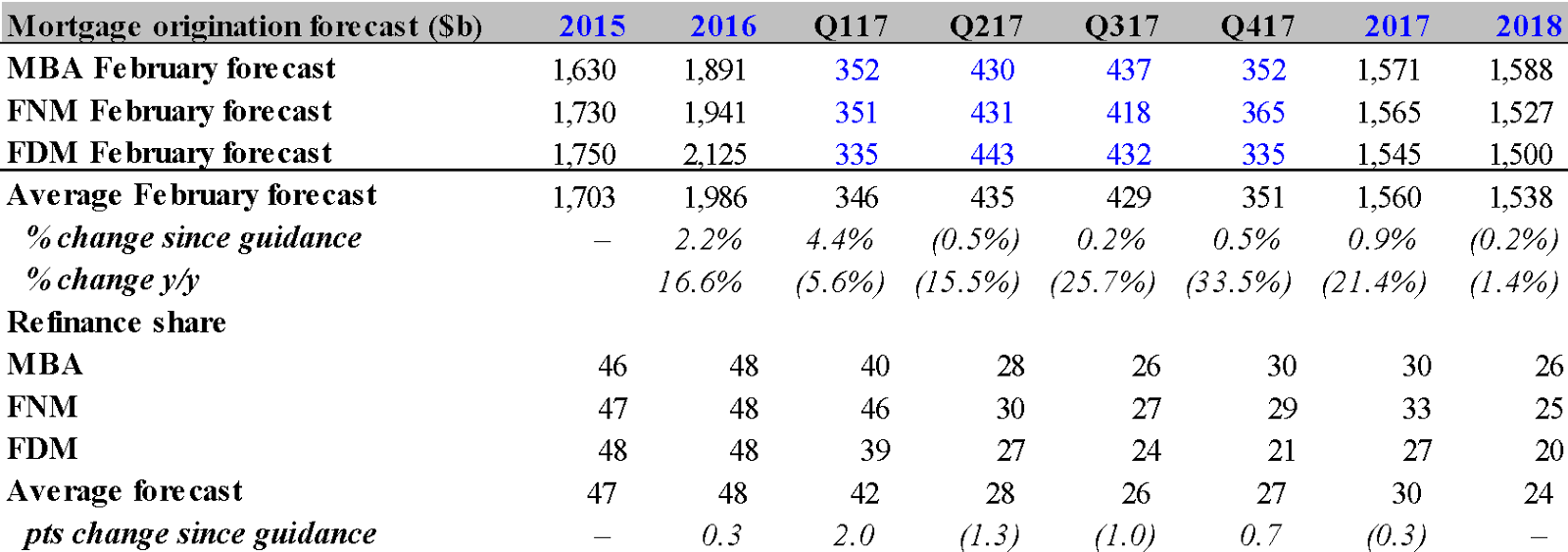

Interest rate and refinancing concerns overblown: There has been a lot of concern from bears that declining refinancing mortgage origination volumes could cause ELLI to under deliver on revenue growth. We think these concerns are overrated. ELLI has 90% visibility in its 2017 revenue guidance. 60-70% of its revenue comes from SaaS contracts and are recurring, 20-30% from Mortgage Returns, All Regs, baseline Network revenue, and other transactional revenue which didn’t go away even when mortgage volumes dropped 38% in 2014 to the trough levels. Only 10% of its revenue is truly variable, which consists of SBP Success Fees and Variable Network revenue. ELLI currently has no exposure to the top five banks. In addition, ELLI just started a new vertical for construction loans, which can drive 5 to 7% of the loans that ELLI do currently. We think it will offset some of the volume declines in refi. These loans will go through the same system, and will be eligible for success based pricing. Big money-center banks have relatively higher share of the refi market, therefore, ELLI has been relatively underweight refis versus new purchases and less exposed to the refi activity than people think. The company generally has elevated marketing expenses in Q1 due to a user conference. Operating leverage should be much better throughout the rest of the year and in 2018. Only about 7% of cost-of-goods is variable. By 2021, we think the company can earn over $8.00 per share of EPS. This is not even factoring in optionality for the company to enter new verticals like auto loans or servicing or win a mega deal with a top 5 bank. The chart below shows how ELLI grew 25% in 2014, which was the trough year for mortgages.

Source: MBA, FNM and FDM

Source: Ellie Mae

-

Upside to 2017: We think the guidance is conservative for the next year, given contractual price increases, active seats going up, new construction loan vertical adding to volumes and the growth in the purchase volume and the market share shift. We also think that the street is not understanding the operating leverage in the business properly this year. We think there is a 3% and 8.5% upside to FY17 revenue and EBITDA, respectively. The origination market is tracking 4% better than originally forecasted by the agencies (see the chart below) for the quarter.

Source: MBA, FNM and FDM

-

Great management team and culture

-

Checks suggest great customer satisfaction, strong competitive position and innovative culture at the company. It has been consistently rated as one of the top places to work in Silicon Valley. CEO Jonathan Corr is considered a visionary in the mortgage industry, and has received numerous awards in Silicon Valley for his leadership. We also like the CFO, Ed Luce, who has consistently over delivered on the Company targets and has executed flawlessly on the strategy. Ed is retiring in April, and will stay throughout the year to make a smooth transition.

Valuation:

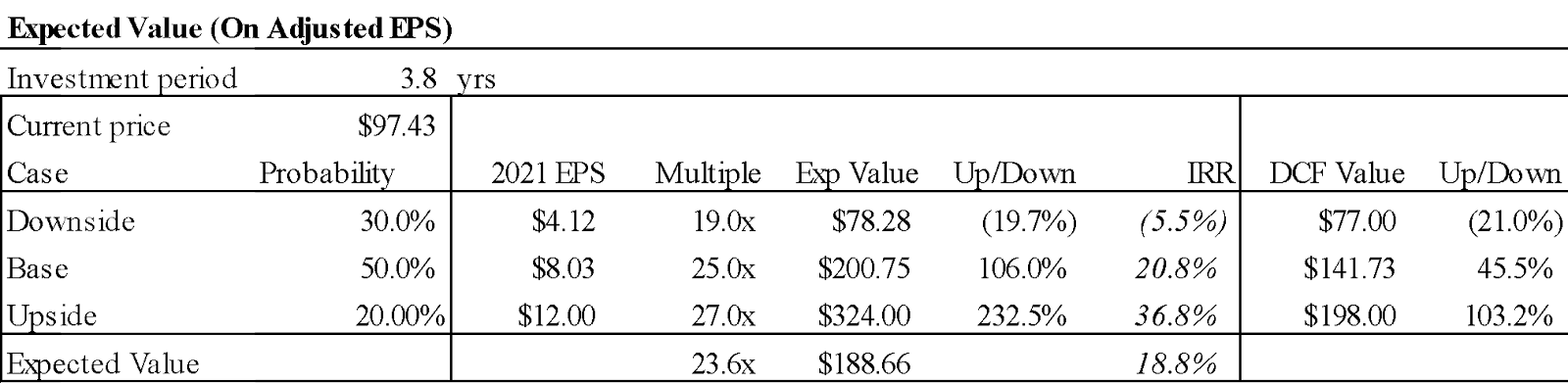

Since ELLI is a compounder we value it on a 5 year basis. In the base case, we assume ELLI’s penetration reaches 46% of the mortgage origination seats (excluding big banks) and revenue per active encompass user reaches 2.2x the 2016 number in the next 5 years. We estimate adjusted EBITDA margins in the high 40s to get to our base case of $8.0 EPS. At a 25x multiple, that results in a 106% upside or a 21% IRR for the next 4 years. In the downside case, we assume ELLI’s penetration reaches only 35% of the mortgage origination seats and revenue per active encompass user reaches 1.7x the 2016 number. We estimate adjusted EBITDA margins in the high 30s to get to our downside case of $4.12 EPS. At a 19x multiple, that results in a -20% downside in the next 4 years. In the upside case, we assume ELLI’s penetration reaches 52% of the mortgage origination seats and revenue per active encompass user reaches 2.4x the 2016 number. We also assume $113mm of incremental revenue from a new vertical. We estimate adjusted EBITDA margins of mid 50s to get to our upside case of $12.00 EPS. Our DCF values the company as of today assuming a 9% cost of capital. We subtract stock comp and R&D capitalization in the DCF. At the current price, we find the risk-reward really appealing in ELLI.

Key Risks:

-

Competition:

-

In sourcing of origination software internally by the clients.

-

Competition from Byte Software (CBCInnovis); Calyx Technology; DH Corporation; LendingQB, Mortgage Builder Software (Altisource Portfolio Solutions); Mortgage Cadence(Accenture); Wipro Gallagher Solutions; LoanSphere Empower and LoanSphere LendingSpace (Black Knight).

-

Growth slow down

-

Refinancing: The increase in the federal funds rate may cause mortgage interest rates to rise. Increases in mortgage interest rates could reduce the volume of new mortgages originated, in particular the refinancing volumes which are more sensitive to interest rates. 30% to 40% of ELLI’s revenues have some sensitivity to mortgage volumes. However, 90% of revenues are visible in a given year. In other words, if originations reached a similar level as the trough in 2014, 90% of Ellie Mae’s revenues will be intact. In 2014, when originations were down -38%, ELLI’s revenues were still up 25%.

-

Low household formation leading to lower purchase volumes.

-

Inability to grow Ellie Mae Network and the add-on services.

-

Longer and more expensive sales cycle resulting in a lower booking of seats missing street expectations.

-

High seat attrition or renewal at lower rates.

-

Regulatory risk

-

Changes in current legislation or new legislation, increasing costs by requiring ELLI to update its products and services. The failure of its products and services to address relevant laws and regulations could adversely affect its business.

-

Potential structural changes in the U.S. residential mortgage industry, in particular plans to diminish the role of Fannie Mae and Freddie Mac, could disrupt the residential mortgage market and have a material adverse effect on ELLI’s business.

-

Technology and security risk

-

Hacking

-

Network downtime

Appendix (taken from 10k and recent investor presentations)

Company overview:

ELLI is a leading provider of SaaS mortgage origination platform for the lenders. ELLI’s Encompass all-in-one mortgage management solution provides one system of record that allows banks, credit unions, and mortgage lenders to originate and fund mortgages and improve compliance, loan quality, and efficiency. It handles most of the functions involved in running the business of originating mortgages including: customer relationship management; loan processing; underwriting, preparation of mortgage applications, disclosure agreements, and closing documents; funding and closing the loan for the borrower; compliance with regulatory and investor requirements and overall enterprise management that provides one system of record for loans. Delivery of ELLI’s Encompass software in a SaaS environment provides customers with the added benefits of lower up front implementation costs and reduced need for an infrastructure of servers, storage and network devices as well as the staff needed to support the infrastructure. Moreover, SaaS Encompass provides access to the most current version of the software, including periodic upgrades and regulatory updates. ELLI also hosts the Ellie Mae Network, a proprietary electronic platform that allows Encompass users to conduct electronic business transactions with investors and service providers they work with in order to process and fund loans.

ELLI offers Encompass users a variety of other on-demand software services, including: Encompass CenterWise, a bundled offering of electronic document management, or EDM, and websites used for customer relationship management such as Encompass WebCenter and Encompass TPO WebCenter; Encompass Compliance Service, which automatically checks for compliance with federal, state, and local regulations throughout the origination process; Encompass Docs Solution, which automatically prepares the disclosure and closing documents necessary to fund a mortgage; Encompass CRM, currently operated under ELLI’s Mortgage Returns brand, which offers a suite of sales and marketing tools to manage contacts, leads and marketing campaigns; Encompass Product and Pricing Service, which allows Encompass users to compare loans offered by different lenders and investors to determine the appropriate mortgage programs available to a particular borrower; Encompass Flood Service, which allows Encompass users to order and transfer flood zone certifications; Encompass Consumer Direct, a web-based tool that allows borrowers to complete a loan application online; Total Quality Loan, or TQL, which offers the following suite: Encompass Fraud Service, which enables fraud detection, valuation, validation, and risk analysis services using streamlined workflows and processing rules; Encompass 4506-T, a tax transcript service which provides income verification capability to ELLI’s customers; and Encompass Appraisal Service, a service for ordering and managing appraisals; and content and services under ELLI’s AllRegs brand, which includes research and reference, education, documentation, and data and analytics products relating to the mortgage industry. For the lenders, investors and service providers on the Ellie Mae Network, ELLI provides electronic connectivity that allows them to do business with mortgage origination professionals using Encompass.

Mortgage originators pay for SaaS Encompass in one of two models: recurring monthly subscription fees or monthly fees based on the number of licensed users and mortgages funded, which ELLI refers to as Success Based Pricing. The base fee is $85 per month per seat for a new customer, and if the customers do above a certain loan amount, they pay ELLI a success fee. Contracts are generally for 3-5 years, moving towards an average of a 3 year duration. ELLI’s additional services are paid on a subscription or transaction basis. Lenders and service providers participating in the Ellie Mae Network also pay it fees, generally on a per transaction basis, for transactions processed through the Ellie Mae Network from Encompass users.

Under the AllRegs brand, ELLI’s research and reference products include single and multifamily underwriting & insuring guidelines as well as libraries of federal and state laws and regulations. In addition, ELLI is the exclusive electronic publisher of Fannie Mae’s and Freddie Mac’s Single and Multi-Family Seller/Servicer Guides and The Federal Home Loan Bank’s Mortgage Partnership Finance, or MPF Program Guidelines. ELLI’s educational division, AllRegs Academy, offers courses related to the mortgage industry, including self-paced training, instructor-led online courses, webinars or live classroom training, and certified continuing education classes for state licensed mortgage originators. In addition, through the AllRegs brand, ELLI offers documentation and learning management solutions to facilitate ELLI’s customers’ mortgage lending compliance, as well as data and analytics services relating to investor loan products. The chart below shoes how the mortgages used to be done conventionally historically, and the efficient ELLI process.

Source: Ellie Mae

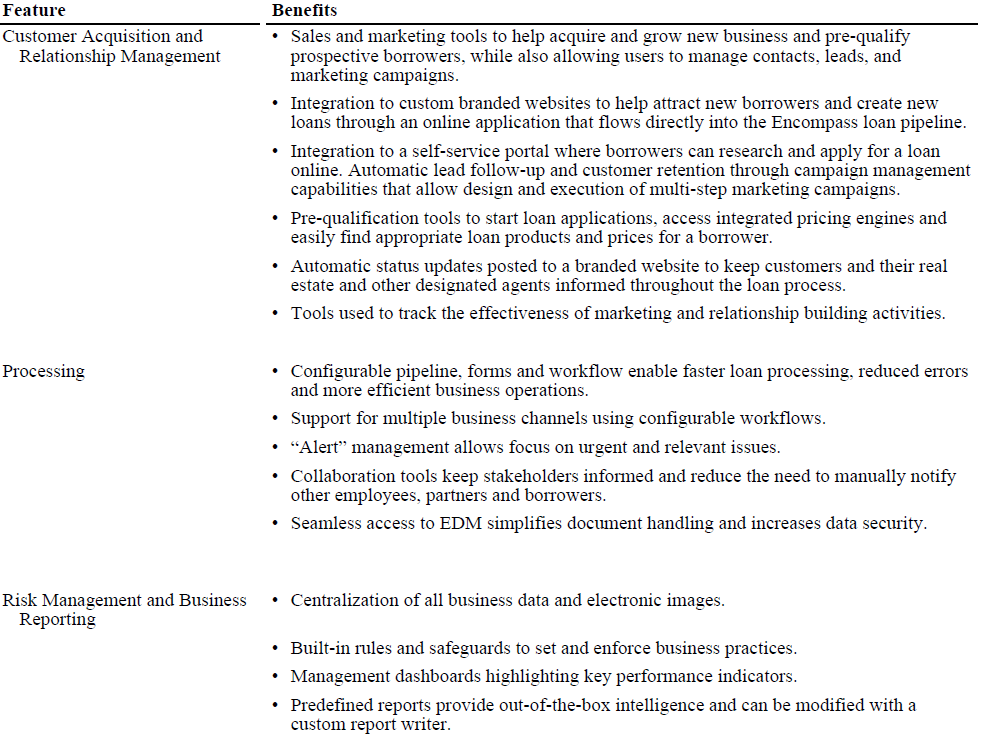

Products and services:

Encompass provides the following features and benefits:

Source: ELLI investor presentation

TAM math

There are currently 850,000 total mortgage professionals, out of which 25% are ELLI’s contracted users. These seats do not include the top five banks in the US, which have another 200,000 seats. This number has changed from 500,000 a few years ago because of the growth in the market since the great recession, and because of better reporting through National Mortgage Licensing Service (NMLS). Under regulation, all loan officers now need to register with NMLS, and have to pay a fee to renew it every year. A recent number quoted by MLS for loan officers was 535,000 (updated every few months), but it covers only the front end of the business. Currently in the mortgage workflow, there is about a 50/50 ratio of front-end to back-end people, such as compliance, underwriting, bosses looking in on the pipeline, accountants, auditors, securitizers, who don't need to buy a license and therefore don’t need to register with NMLS. Out of ELLI’s database of 215,000 users, back-end positions have a 1-for-1 ratio with front-end positions. It was a 2-for-1 ratio as recently as a couple years ago before everyone started hiring compliance teams on the back side of that process. If ELLI just maximizes these 850,000 (Currently has 180k) users with its current revenue per seat, it can generate $1billion in revenue per year. Maximizing the adoption among these users could result in $6.25bl in revenue vs. $250mm in revenue last year.

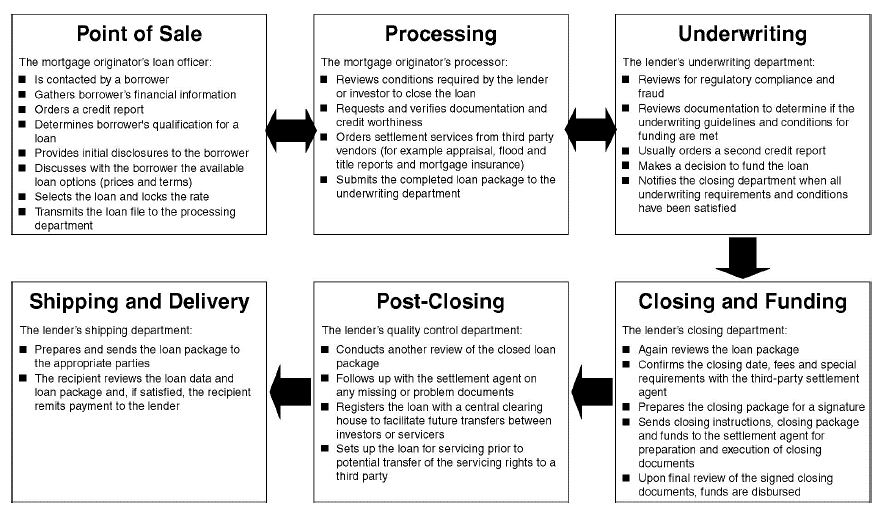

Origination process

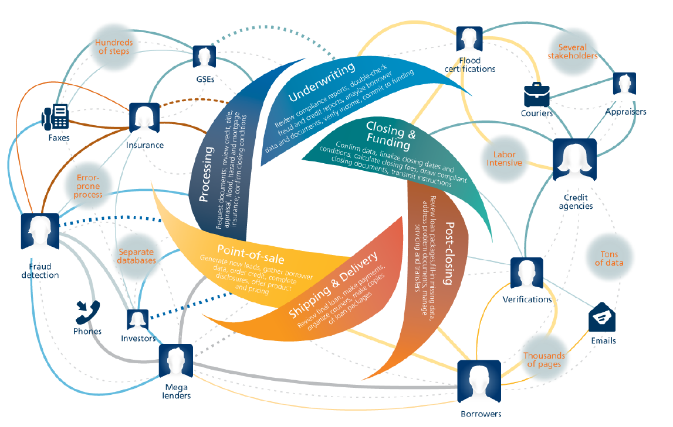

Originating a residential mortgage involves multiple parties and requires a complex series of data-laden transactions that must be handled accurately under tight time constraints. By the time a mortgage has been funded, a typical loan package contains over one thousand pages of documents that come from over a dozen different entities, usually operating on disparate technology systems and databases. Traditionally, much of the data used to prepare these documents has been gathered manually, rather than electronically, with documents exchanged among the many participants by facsimile, courier or mail. The entire process results in significant duplicative efforts, time delays, errors, costs, and redundant paper documentation, often exposing borrower data to potential privacy and security breaches. The following diagram of the mortgage origination process provides a framework for understanding the complexity and inefficiency of the process and the need for automated solutions. In addition to the challenges involved in processing loans, mortgage originators must satisfy a multitude of federal, state and local regulations, and address basic business needs, including marketing, sales, product fulfillment, customer support, reporting, and general management functions. Historically, most mortgage originators have operated their businesses using separate task specific software applications that were interconnected, if at all, through customized integrations. This often resulted in constraints on effective collaboration among operating departments, limited ability to monitor the business comprehensively, increased risk of error due to inconsistent data, failure to incorporate current regulations into work flows, inadequate security and control over the process, and expensive technical integration and maintenance costs.

Increased Regulation Affecting Lenders and Investors

The residential mortgage industry continues to evolve and undergo significant changes. There are five major regulation mentioned below that are currently impacting the residential mortgage industry:

-

Regulation Z of the Truth in Lending Act of 1968 (TILA) by CFPB, with an effective date for applications taken on or after January 10, 2014, in which the CFPB implemented amendments to TILA made by the Dodd-Frank Act, to require that creditors determine a consumer’s ability to repay a mortgage before making a loan and to establish both minimum mortgage underwriting standards and standards for complying with the ability to repay by defining a “qualified mortgage.”

-

Both Regulation X of the Real Estate Settlement Procedures Act of 1974 (RESPA), and Regulation Z of TILA, with an effective date for applications taken on or after January 10, 2014, in which the CFPB implemented amendments to RESPA and TILA made by the Dodd-Frank Act to expand the types of mortgage loans that are subject to the protections of the Home Ownership and Equity Protection Act of 1994, or HOEPA, by revising and expanding the triggers for coverage under HOEPA, and to impose additional restrictions on HOEPA mortgage loans, including a pre-loan counseling requirement.

-

Both Regulation X of RESPA and Regulation Z of TILA, in which the Dodd-Frank Act directs the CFPB to issue proposed rules and forms that combine certain disclosures that consumers receive in connection with applying for and closing on a mortgage loan. In response, the CFPB issued the TILA-RESPA Integrated Disclosure or Know Before You Owe (TRID or KYBO) rule with an effective date for mortgage applications taken on or after October 3, 2015. In addition to combining the existing disclosure requirements and implementing new requirements in the Dodd-Frank Act, the final KYBO rule provides extensive guidance regarding compliance with those requirements. As of today, lenders are still focused on TRID. Lenders not using Encompass have had to design manual workarounds and incur significant man hours to correct problems causing higher cost to close a loan than their competitor

-

Section 15G of the Exchange Act (15. U.S.C. 78o-11), as added by the Dodd-Frank Act, with an effective date for applications taken on or after December 24, 2015, in which the Federal Reserve Board, the SEC, and the Department of Housing and Urban Development implement credit risk retention requirements for asset-backed securities. The final rule generally requires securitizers in both public and private securitization transactions to retain no less than 5% of the credit risk of the assets collateralizing any asset-backed security issuance. The final rule includes a variety of exemptions from these requirements, including an exemption for federal government sponsored residential mortgages and asset-backed securities that are collateralized exclusively by residential mortgages that qualify as “qualified residential mortgages." The final rule’s definition of "qualified residential mortgage" is the same as the definition of “qualified mortgage” under the CFPB’s ability-to-repay rules.

-

Regulation C to implement amendments to the Home Mortgage Disclosure Act, or HMDA, published in the Federal Register October 28, 2015, in which the Dodd-Frank Act directs the CFPB to add several new reporting requirements and to clarify several existing requirements to HMDA. The CFPB is also proposing changes to institutional and transactional coverage under Regulation C.:

-

Regulation C will be starting in 2017 and will be focused on:

-

How institutions collect, report, and disclose information about their mortgage lending activity.

-

Change to the types of institutions and transactions subject to the regulations, as well as the information that must be collected, recorded, reported, processed, and disclosed.

-

Starting in 2018: Implementation of Appendix A of HMDA

-

Lenders will be required to report using a web based submission tool.

-

Will also have to report additional information about loans applied for, originated, and acquired. More changes coming down the pike.

There are regulatory/compliance changes occurring every month, not only the “big ones” (e.g. TRID/RESPA TILA). In Q1 2016, the government revised its definition of “application” for reporting loan applications plus other reporting changes related to application amounts.

In addition to the regulatory reforms that have been introduced or proposed, other significant changes in regulations have been implemented since 2008 that are subject to regulatory enforcement, including material changes to Regulation Z of TILA by the Federal Reserve Board to protect consumers in the mortgage market from unfair or abusive lending practices that could arise from certain loan originator compensation practices by prohibiting payments to loan originators based on the terms or conditions of the transaction other than the amount of credit extended. These regulatory reforms further complicate the process and increase the amount of documentation required to originate and fund residential mortgages.

Lenders have eliminated many high-risk loan product offerings and significantly tightened underwriting and processing requirements. Similarly, investors seek higher-quality, lower-risk loans in which to invest. Consistent with these tightened standards and expectations, lenders and investors are demanding increased levels of documentation of the data upon which a lending decision will be based, increased use of third-party services to obtain unbiased and independent verification of borrowers’ creditworthiness, greater proof of the adequacy of the collateral securing mortgages and strict compliance with regulatory requirements. This trend further increases the amount of documentation and number of services required to originate and fund residential mortgages. Increased enforcement by federal and state regulators continues to encourage mortgage originators to explore technology solutions that provide adequate controls and policy enforcement to facilitate originating compliant loans.

ELLI expects costs to continue to be a significant consideration for mortgage originators due to continued increased regulation and heightened quality standards. As a result, mortgage originators have sought to increase their efficiency and reduce fixed expenses, leading them to explore technology solutions to automate their business processes as well as methods to avoid or reduce expenses that are not tied to revenue generating activities.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Catalysts / Path to Value Realization:

Upside in stock will come from:

-

Earnings beat through growth and margin expansion

-

Revenue per seat expansion at a faster rate than the street, and the street realizing higher base fees per seat

-

Long term margin guidance increase at the analyst day on March 7th

-

Upside option: Incremental growth from new products, higher than expected market share gains and higher base pricing. Winning a mega bank deal.

| show sort by |