| 2018 | 2019 | ||||||

| Price: | 7.62 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 1,205 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 9,182 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- compounder club

Description

Altice – February 2018:

We believe an investment in Altice NV (Euronext ticker: ATC) is the optimal way to buy Altice’s US subsidiary (ATUS) while acquiring Altice’s deeply undervalued non-US business for a pittance. After Altice NV spins off its ownership of Altice USA over the next few months, ~75% of your purchase price will be returned in shares of ATUS. In anticipation of the spinoff and by dint of its association with the loathed European half of Altice, the US shares have sold off substantially. On a standalone basis, we believe Altice USA is the most attractively priced major US cableco. Further, the remaining Altice Europe stub is being given away, priced as if the company is likely to go bankrupt. This is despite the fact the entire credit stack trades at or near par. The European stub is highly convex and has a clear path to significant upside scenarios if things simply are not terrible (which they aren’t).

Without heroic assumptions, we believe there is a clear path to $30+ per share in ATUS (including a near term 10% special dividend) and the post-spin European stub (ATC) can be a multi-bagger. Both trade at large run-rate equity free cash flow yields.

-----

Altice NV is the holding company for a variety of global telecom (cable, mobile) and content assets. It is majority controlled by Swiss Franco Israeli entrepreneur Patrick Drahi.

Altice is loathed. Its stock is down ~70% over the past several months and even more since its summer 2015 peak. The proximate cause of the recent declines was an underwhelming Q3 2017 earnings report in its French subsidiary and the associated loss of confidence in management’s turnaround plan working in the near term.

The business can be simplified by viewing it as:

-

U.S.A.

-

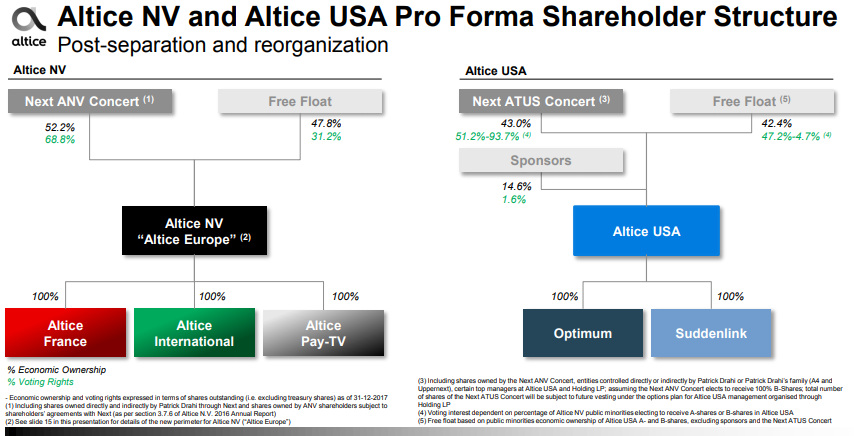

Within US, Altice owns 70.5% of Altice USA, which itself is a public company (ticker: ATUS), which is worth ~86% of the ATC market cap1. This value needs to be reduced by the $1.5 billion (€1.2 billion) dividend Altice USA is paying simultaneous to the spin-off. Post-spin, Altice NV will still effectively own 3.3% of ATUS (distributing the other 67.2% to Altice NV shareholders).

Billions

|

Altice NV Market Cap @ €8.00 |

€ 9.6 |

|

less 70.5% ATUS Stake @ €16.13 |

-€ 8.4 |

|

Implied Altice NV Equity Value |

€ 1.2 |

|

plus pre-spin ATUS special dividend |

€ 0.9 |

|

plus 3.3% retained ATUS Stake |

€ 0.4 |

|

Pro Forma Altice NV Market Cap |

€ 2.5 |

-

Non-US.

-

Currently, the implied market cap of the non-US business is €1.2 billion. If you add in Altice’s 70.5% share of the dividend (worth ~€0.85 billion) and its 3.3% ownership of ATUS (€0.35 billion), the stub will be worth €2.5 billion.

For simplicity, I will refer to Altice NV non-US as “Altice Europe”. Both Altice USA and Altice Europe generate substantial free cash flow. The spin-off is scheduled to occur by the end of Q2 2018.

The Altice complex is among the cheapest large businesses we can find. We believe Altice USA is a very attractive investment. Further, the non-US stub seems unusually cheap, and can be created at a massive free cash flow yield while minimizing downside risks. If you want to own ATUS, you should do this through ATC, which comes with Altice Europe equity being valued as a very low cost, very long-dated option on not going bankrupt. Given a credit stack trading near par, it seems “not going bankrupt” is fairly likely.

-----

Altice High Level:

Altice is the result of a rollup. During the 2000s, Altice rolled up 99% of French cable assets (this sounds more impressive than it is, given cable was only 10% TV share in France). Altice subsequently acquired and developed telecom and content assets in a variety of markets, including Israel, the Dominican Republic, more in France, Portugal, and the US.

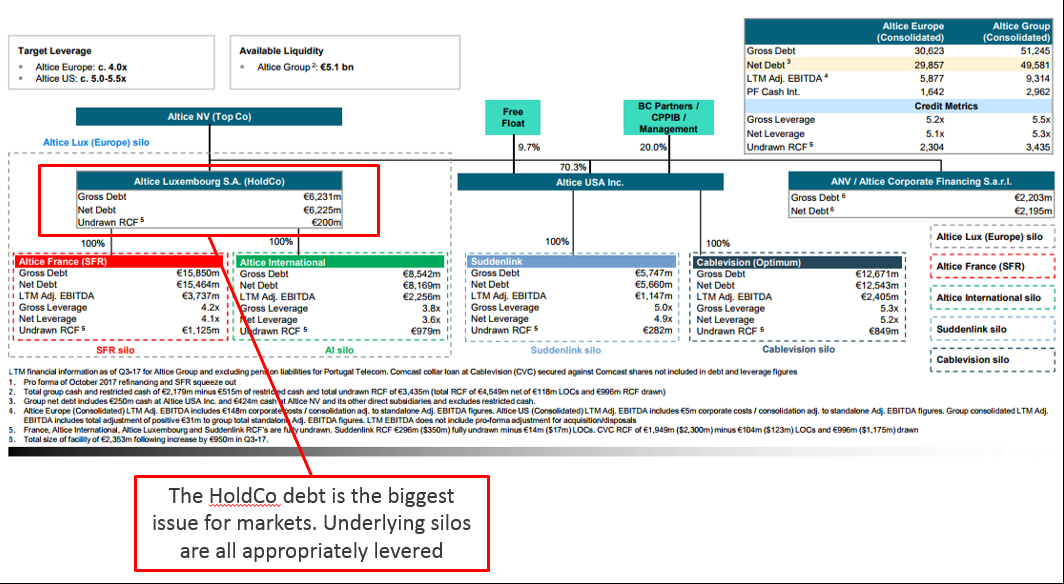

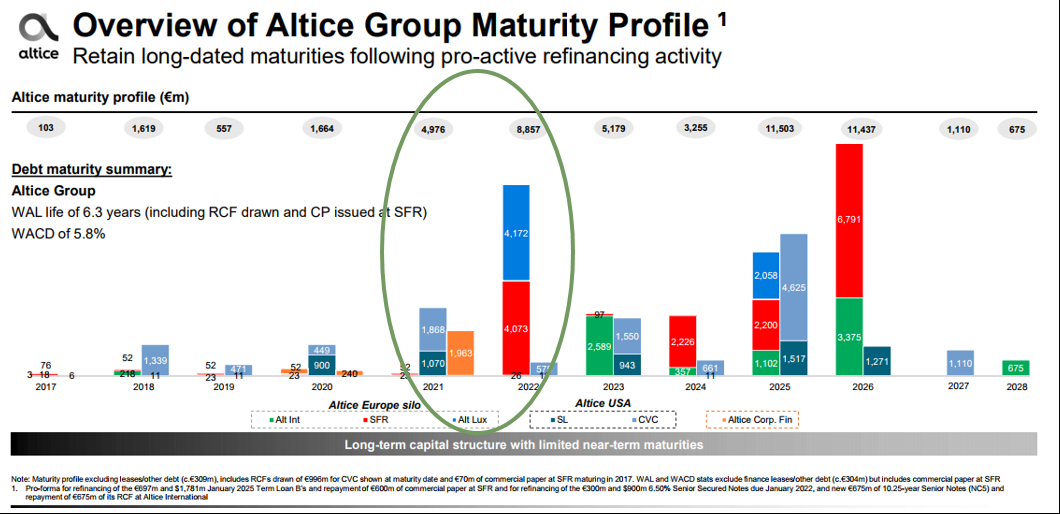

Given the non-US business is being sold for a pittance, one might assume it is distressed. You would be wrong. Altice has a complex capital structure, which I’ve copied below, but it is trading at or above par across the whole capital stack, except for the Luxembourg HoldCo (which currently owns the non-US assets), which is trading in the 90s. Altice NV and its subsidiaries have no meaningful maturities outside the US until 2021/22.

Further, both the US and the non-US business generate substantial “after everything” free cash flow today. Unlike Charter, which is an “it’s cheap on 2021 free cash flow” story, Altice USA and Altice Europe are trading at double digit after-everything trailing equity free cash flow yields today…and we believe 2021 free cash flow stands to be much higher.

-----

The Investment Setup:

Note: I am going to use euros as my primary currency with a 1.24 Fx rate, unless otherwise noted. Data from mid-February 2018.

The preponderance of an investment in ATC will be returned by an ownership stake in ATUS in a few months. As of today, Altice NV’s ownership of ATUS is worth 86% of the purchase price of ATC. Post-spin, you will own ATUS shares and the remaining Altice Europe “stub”, both of which we believe are dramatically undervalued. In particular, the stub equity is priced as if Altice Europe will likely go out of business. The stub has exceptional convexity to things simply not going terribly.

Altice NV’s market cap is €9.6 billion (given an €8.00 share price). PLEASE NOTE: Bloomberg uses an errant share counts that includes Treasury shares that are being retired. The correct share count is ~1.205 billion shares.

Altice USA’s market cap is $14.7 billion / €11.9 billion (given a $20.00 share price), pre-dividend. Deducting the $1.5 billion dividend gives a pro forma post-spin market cap of $13.2B. That equates to €10.6 billion post-spin market cap. NV owns 70.5% of ATUS, worth €7.5 billion (post-dividend).

Altice non-US stub value is therefore €1.2 billion pre-spin and €2.5 billion post-spin. This delta is the result of a few moving parts: 1) NV will receive €0.85 billion of dividend, of which it will keep €200-300 million in cash (and use the balance to pay down debt). Via a spinoff, Altice NV is distributing 67.2% out of its 70.5%, leaving it with 3.3% ownership of ATUS. In sum, the ATC implied trading price should be: €1.2 billion current non-US stub value + the 3.3% ATUS ownership worth €0.35 billion + €0.85 billion of dividend = ~€2.5 billion implied market cap (~€1.9 billion of which is pro forma cash and ATUS stock). It’s debatable whether or not Altice NV’s post-spin market cap will get credit for these moving parts, but this is directionally accurate.

On a Q3 run-rate basis, Altice non-US generates ~€1.0 billion of pre-tax equity free cash flow (EBITDA – CapEx – Interest Expense), implying a massive free 40%-100%+ pre-tax cash flow yield on the non-US portion of the stub (depending on your calculation methodology). While we believe buying Altice NV outright today is attractive, one could choose to short out ATUS and buy CDS for a single digit running cost and create the NV stub, while mitigating bankruptcy risk at the same time. This would create tremendous upside convexity, though it would require balance sheet capacity.

We are not shorting the US because Altice USA is arguably the most attractive US cableco, generating near-industry leading EBITDA and FCF margins. Altice USA is continuing to grow topline and expand margins, and it trades on double digit free cash flow yields (Q3 annualized). In essence, we believe ATUS is a very attractive investment and we can create it through NV while owning a cheap option on the non-US and any future value creation.

As mentioned above, one might assume that Altice is in distress given NV’s stub trades for so little equity value. The most levered part of the capital structure is a Luxembourg HoldCo that sits between NV and its two non-US telco credit pools: Altice France (SFR) and Altice International (primarily Portugal, Israel, and the Dominican Republic). However, the Lux HoldCo debt trades in the 90s:

Note that there are no HoldCo maturities until 2022. The 2022s are near par and become callable at a premium beginning this year (and can be called at par in 2020).

-----

Background and Description:

Patrick Drahi was, until two years ago, largely unknown to US business people and investors. He and his partners (including Armando Pereira) founded Altice in the early 2000s to roll-up the French cable industry. Drahi is a Moroccan born Franco-Israeli entrepreneur who lives in Switzerland. He and his partners still own over 50% of Altice (even more on a voting basis), making him one of the richest people in the world. In his first entrepreneurial incarnation, Drahi built and operated businesses related to French cable in the 1990s, before selling to John Malone’s UPC at the end of the decade (UPC is now part of Liberty Global, also effectively controlled by John Malone). French cable at that time was highly fragmented by regulatory decree, preventing any one player from achieving necessary scale. With no French cable company achieving scale, its collective network infrastructure suffered from underinvestment. As a result, other forms of pay TV came to dominate France with cable serving less than 10% of the population. Likewise, France’s broadband industry came to be dominated by DSL, a structurally inferior service when compared to fiber solutions, including cable.

At the same time Drahi formed Altice, French regulations changed allowing for cable consolidation. In a remarkable four year period, Altice acquired virtually every French cable company, ultimately taking control of 99% of the industry (with private equity backing initially from Cinven and later Carlyle). This business was called Numericable.

Altice went on to build and acquire primarily fixed and mobile telco assets in Belgium, Portugal, Swtizerland, the French Overseas Territories, the Dominican Republic, Israel, and – most recently – the United States. Altice and Numericable both IPO’d in the past four years (Altice ultimately bought out all of Numericable, which was renamed SFR after it acquired the much larger SFR a few years ago).

After a successful IPO three years ago, Altice increased the scale and geographic range of its acquisition spree, closing four large acquisitions and several more modest deals in a three year period. In succession, it bought SFR (France’s #2 mobile player with a large white labeled DSL presence), Portugal Telecom (incumbent telco - #1 in fixed and mobile, aka MEO), Suddenlink (top ten US cableco with regional positions in the South and Midwest), and Cablevision (4th largest cableco in US, with leading position in NY tri-state). It also purchased and built several modest content businesses and purchased the national distribution rights for the next several years to a handful of sports (e.g., European Champions League soccer for France).

While Altice is loathed today, Patrick Drahi and his team have been incredible value creators over time. However, you do not have to believe in their value creation skills to find Altice attractive today. You simply need to believe they are rational and will not actively destroy value. For those that do believe Drahi is a value creator, the sword clearly has a double edge in that he is a liberal user of credit markets. This has reduced margin for error, and introduced a level of stock price volatility that I think even he was not truly prepared for.

For simplicity, and to align with its current credit capital structure, Altice can be thought of in two primary pools, both of which feed up into NV: the US and non-US. Within non-US, NV can be thought of as the 100%2 owner of two primary sub-buckets: France and non-France. Altice NV’s ownership of ATUS is bankruptcy remote from Europe. Altice USA itself is comprised of two credit pools that are bankruptcy remote from each other: Suddenlink and Optimum (fka Cablevision).

A simplified capital structure is laid out below. As you can see, above the various OpCos, there is some Luxembourg HoldCo and FinCo/Corporate debt as well. The Lux HoldCo debt has been the primary area of heartburn for the markets.

Take the Lux HoldCo’s 6 ¼ Feb 2025s as an example. Following the Q3 2017 announcement, they fell ~18 points from 111 to 93 and have bounced around since then. This Lux HoldCo debt sits between the European OpCos and NV. In aggregate, the Lux HoldCo debt adds 1.3x turns of net debt/EBITDA to the non-US assets and is the focus of current deleveraging.

Post spin, the capital structure is being realigned with the creation of Altice PayTV, which takes many of the cash burning content assets out of the OpCo and Lux (HoldCo) credit pools. We view this as substantially credit enhancing for the HoldCo.

Since reporting its soft Q3 (more on that below), Altice has announced its intention to deleverage the non-US credit pools through free cash flow and selective divestments. I can debate the merits of this decision, but I believe Drahi still believes there is a significant consolidation opportunity and that he cannot pursue it until he calms capital markets.

As noted, this capital structure has several moving parts in conjunction with the spinoff. The credit silos are changing, and Altice NV is paying down some of its FinCo debt, while adding liquidity to the NV balance sheet. Below is a summary of the moving parts:

-

USA:

-

Most of NV’s stake in the US is being spun off to NV shareholders;

-

The US stops paying NV a management fee (~$30mm p.a.).

-

The US also buys Altice Technical Services USA from Altice International for a de minimis amount;

-

The US pays a $1.5B one-time dividend immediately prior to the spin;

-

Via Altice NV’s 70.5% ownership of Altice USA, it will receive ~€0.85 billion of dividend proceeds:

-

~€0.6 billion of that will be used to pay down FinCo debt;

-

The balance will be held on balance sheet, primarily to fund Altice PayTV (see below);

-

France and International will be swapping assets to better align with their geographic operations and reduce intercompany adjustments from well over €1 billion p.a. to closer to €100 million

-

France is buying French Overseas Territories (FOT), France’s Altice Technical Services (ATS), and Intelcia (customer care centers) for €550 million (they generated ~€105 million of EBITDA, so <5.5x purchase price). €300 million is cash and the rest is a seller’s note

-

International receives €550 million (see #3) from France for FOT, ATS-France, and Intelcia, of which €300 million paid in cash and €250 million in a seller note

-

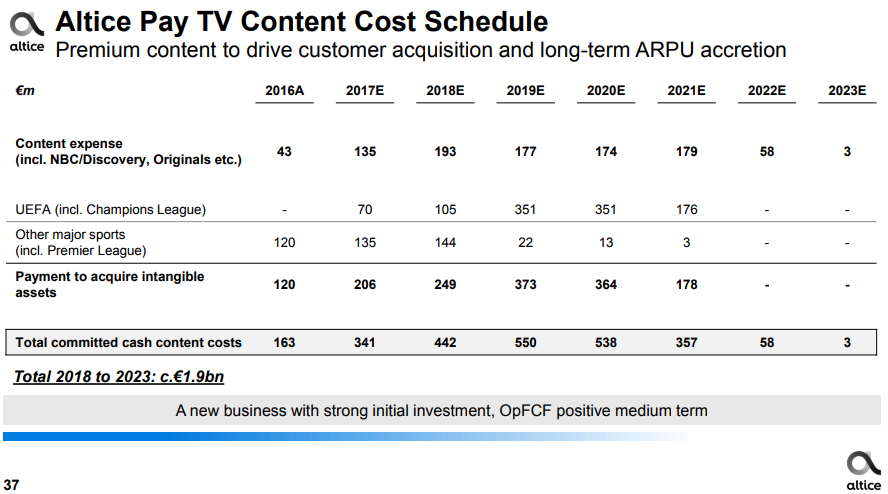

Altice PayTV (APT) is created and will be owned by NV. Importantly, it will live outside of the Lux HoldCo debt perimeter. As discussed below, in addition to “standard” TV content, Altice has invested aggressively (perhaps too much so) in premium content with large annual cost obligations for the next several years. This content was originally contemplated as being exclusive to Altice/SFR. Given SFR’s challenges with subscriber churn, Altice (via APT) now plans to also resell the content wholesale to other video providers (such as SFR’s competitor Orange). SFR is paying APT a one time €300 million fee to escape the high annual fees of the content. It will license that premium content from APT initially for ~€50 million in 2018 (which is well below market) + revenue sharing. I expect the licensing cost will be higher in 2019-2020, reflecting full years of Champions League. APT will also market the content to other providers. APT’s content includes exclusive French rights to European Champions League soccer for three seasons (2018-2021), English Premier League soccer, content from Discovery, and other premium content.

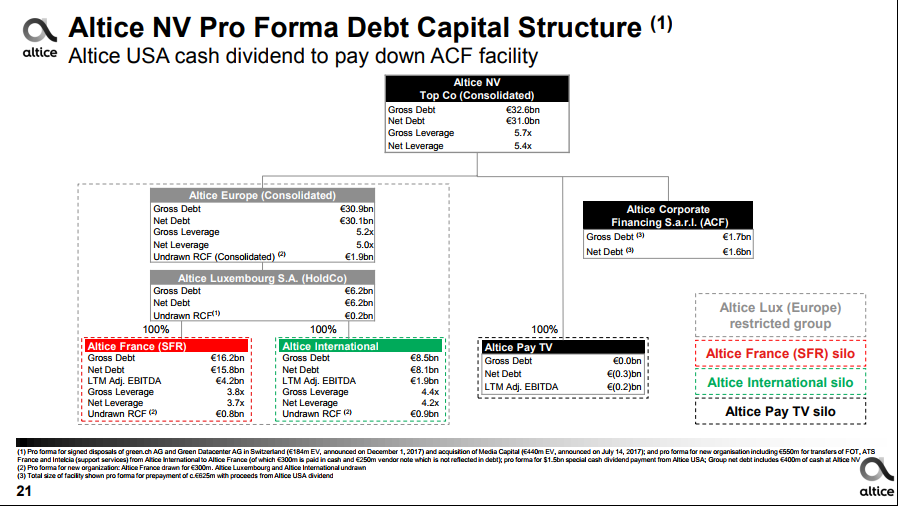

Here is the pro forma credit structure of NV:

With de-levering as a priority, NV has many paths:

-

Free cash flow generation;

-

Cutting low returning growth CapEx in France;

-

Asset sales. Some logical choices:

-

Tower portfolio (France and Portugal have ~18,000 towers, potentially worth €200k+/tower);

-

Dominican Republic business (which is a gem);

-

Wholesale voice business (which is a dog); and

-

Remainder of US holding (NV will still own 3.3% of ATUS on a look-through basis; worth ~€350 million).

-

Note: the above leverage slides include: 1) an already announced and closed sale of its Swiss datacenter business for 10x EBITDA (~€184 million purchase price); and 2) outflow of €440 million for the acquisition of Portugal’s leading TV content (Media Capital), which is under heavy regulatory scrutiny and is iffy to close.

Geographies:

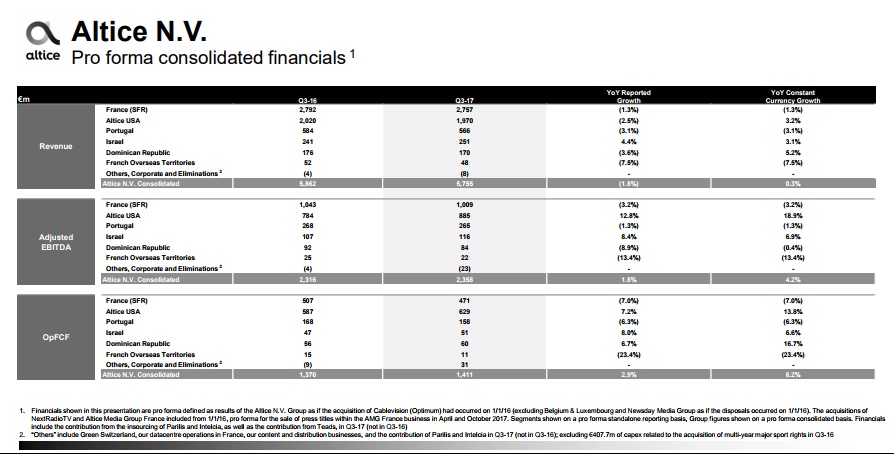

Pre-spin, Altice has three major geographic buckets: France, US, Rest of World. RoW is primarily made up of Portugal, Israel, and the DR. In Q3 2017, here’s how the economics were split up (not adjusting for Altice’s 70.5% ownership of ATUS, which would reduce that proportionately).

On a consolidated basis in Q317 (from the Altice Q3 2017 report):

France: 48% revenue, 42% EBITDA

US: 34% revenue, 37% EBITDA

Portugal: 10% revenue, 11% EBITDA

Israel: 5% revenue, 5% EBITDA

The DR: 3% revenue, 4% EBITDA

Altice is a quad play offering in all markets but the US, where it effectively has no mobile business3. In the DR and Portugal, it is the #1 player and fully converged4. In France, it is #2 (behind Orange) and is fully converged. In Israel, legislation prevents full convergence, requiring mobile and fixed to remain separate. Its Israeli business is branded as HOT Telecom and is a breakeven mobile business and a very profitable fixed business.

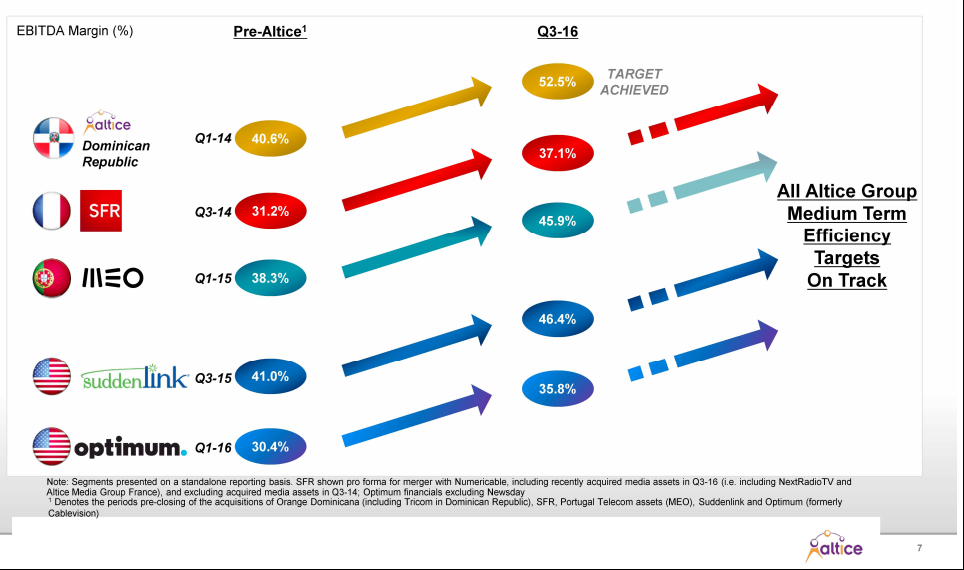

Before entering the US, Altice had a reputation for buying previously stagnant assets for low multiples. They quickly install ZBB and begin to renegotiate contracts with suppliers, often being accused of withholding payments from suppliers during those negotiations. By way of example, when Altice acquired Portugal Telecom, PT had 38% EBITDA margins and was declining 9% top line. Within 18 months (by Q3 16), Altice had stabilized the top line and taken EBITDA margins to 46% (which have continued improving). In our opinion, Altice does this by trading OpEx for CapEx for an initial period of time, fiberizing network and improving 4G coverage rapidly.

This can be seen in Altice’s decision to take Portuguese FTTH and 4G coverage to 100% of all Portuguese homes. Altice has generally been able to do this while still growing OCF (EBITDA – CapEx), reflecting strong cost discipline with the savings used to fund accelerated capital investment. While increasing cash flow and setting a culture of efficiency, Altice chooses to bypass maximizing near term cashflow to increase the duration of cash flow by investing in network. In Portugal, Altice is currently passing nearly 1 million homes per year, having increased its total fiber homes passed from 2.5 million at year end 2015 to 3.9 million as of September 2017. With 5.3 million households in Portugal, Altice is on pace to fiberize the entire nation by 2019. Further, PT has >93% 4G coverage, and is now coming toward a natural end in its 4G push. Future wireless technologies are likely to be built on top of its existing fiber backbone (fiber to the tower, small cell, 5G, etc.), which implies a lower capital intensity as the current projects roll off. We believe CapEx as a percent of sales could decline from the 17-18% range during this peak period to sub-teens, driving massive increases in OCF.

This slide from a year ago highlights the gist of the margin goals. Note that Suddenlink, Optimum, and MEO (Portugal/PT) have continued to improve, but France has struggled in the subsequent year, which is the trigger for the stock price collapse (discussed more below).

Looking Forward:

Altice USA:

We believe Altice USA should generate over €1.0 billion ($1.3+ billion) of pre-tax equity free cash flow in 2018 (Altice USA is not expected to be a meaningful tax payer in 2018). Note, consensus has more than $1.6B of equity free cash flow in 2018. On the conference calls Altice hosted after announcing the US spinout, US CEO Dexter Goei stated that using 2020 consensus numbers, Altice believes the new tax legislation will save them $500 million of cash taxes in 2020 alone. This is an enormous number on a $15 billion market cap.

With consensus adjusted EBITDA at Altice USA expected to be around $4.4 billion in 2018, Altice will end the year at its 5.0x net debt/EBITDA target (note: this does not assume Altice buys back shares, though they have announced a $2.0 billion authorization that activates post-spinoff). On consensus, $4.4 billion 2018 EBITDA, $22B of net debt and $14.8B market cap, Altice USA trades at 8.4x 2018E EBITDA. This is below peers5, despite a much higher FCF conversion profile. At 10x 2018, ATUS would trade near $30/share (vs. ~$20 today), with ongoing consensus EBITDA growth of ~5%.

We believe this US valuation is supported by EBITDA margins gradually expanding to the mid- to high-40s on a blended basis while the top line grows low single digits. Like the rest of the US cable industry, this growth is driven by an attractive mix shift toward higher margin broadband services and away from lower margin TV. Given increased investment in fiber, its new CPE rollout (Altice One), and its recently announced full MVNO with Sprint, CapEx will increase vs. 2017 for a few years, before beginning to decline in 2020.

Our internal view is for slower US growth than consensus, based on a view that ever-growing broadband ARPU is going to be hard to achieve for the industry and that video sub losses could accelerate. We’d be happy to be wrong.

Altice Europe:

We write more about Altice Europe than the US, even though it represents a smaller piece of the purchase price. We believe it could be meaningfully more valuable over time as Portuguese EBITDA margins could pass 50% (vs. 47% in Q3 2017) and France should be able to exceed 40% (vs. 37% in Q3 2017).

We expect very little organic growth for the consolidated top line of Altice Europe, as France continues to work through its churn challenges and Portugal largely maintains its leadership position.

Likewise, we believe Altice Europe is currently in peak CapEx mode, as it finalizes building out its 4G coverage in France and Portugal and is undertaking major fiber to the home (FTTH) upgrades across France and Portugal. As Altice slows its 4G rollout in the next few months, we believe CapEx in those markets will ease. Further, Portuguese fiber spend should slow in about one year, and Altice’s French business (SFR) is giving signals that they may dial back some of their nationwide fiber initiatives (which makes sense to us until the economic performance is proven out).

We believe France is likely to remain a slog during the first half of 2018, before gradually improving into the second half of the year as operations and content offerings progress.

France – What Happened?:

France is a four player mobile market (Orange, SFR, Illiad/Free, and Bouygues Telecom). As bad as the mobile business has been globally, four player markets tend to be particularly competitive when compared to three player markets.

In France, Free (Illiad’s brand) was granted the fourth wireless operator license in 2009, upending what had been a polite oligopoly. Free was granted certain access to Orange’s network infrastructure and has played the role of disrupter, an even more assertive version of T-Mobile’s approach in the US, pricing extremely aggressively to achieve scale. It began with promotions that were €1/month pricing for 2G voice with a plan to build out a more advanced network over time. The three primary incumbent mobile operators (including SFR, which was owned by Vivendi at the time), were built for higher ARPU environments. They began losing customers and reducing ARPU at the same time, destroying the industry’s profit pool. This led to Vivendi putting SFR for sale. It languished on the block for years, as the natural in-market buyers were challenged by the same market dynamics and regulatory restrictions (i.e., Orange already being considered too large).

During this multi-year trip to corporate purgatory, SFR’s formerly well-regarded brand position eroded substantially. Vivendi starved SFR of capital investment for years. By the time Numericable closed its SFR acquisition at the end of 2014, SFR’s competitive positions was challenged. It had terrible 4G coverage (only 1/3 of the country vs. >70% coverage for both Orange and Bouygues), poor customer service, a deteriorating brand, and thousands of unhappy employees now deemed redundant.

On the positive side, Numericable was buying scale – SFR was the #2 mobile and broadband (DSL) player in France - and the ability to sell a converged offer. However, given Numericable’s cable footprint was limited, SFR’s broadband customers could not immediately come on-net and those DSL customers continued to use copper wholesaled from Orange. At the time of acquisition, SFR spent nearly €1 billion a year to lease lines from and pay monthly DSL wholesale fees to Orange. Disappointingly, three years later, SFR still spends €0.8 billion. As SFR pushes fiber deeper and deeper, the need to sublet from Orange will decline.

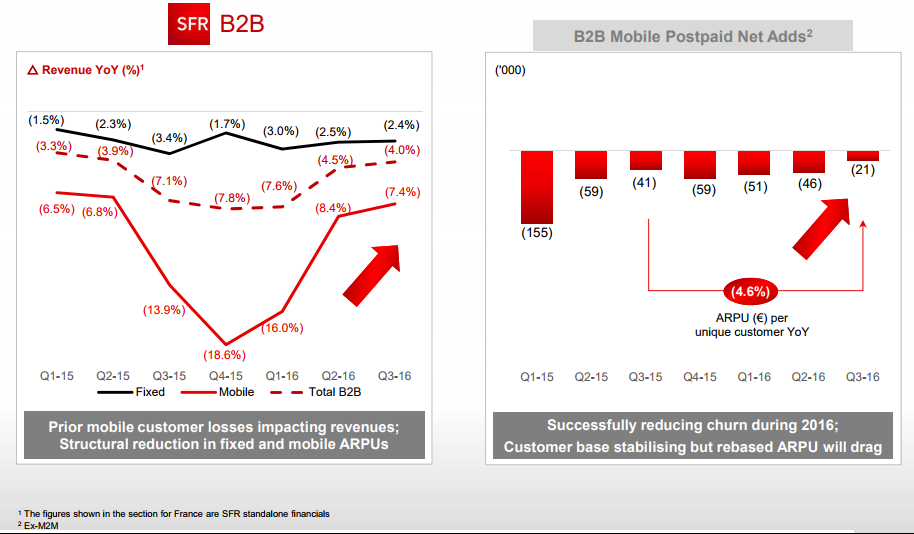

Altice understood that the SFR purchase would involve a significant turnaround, but still dramatically underestimated the challenge. SFR was shrinking top line by >5% p.a. when the deal closed. This was driven by large churn in consumer DSL, consumer mobile, and B2B.

Altice immediately began to invest massively in upgrading SFR’s physical network. First, it needed to catch up on 4G coverage, lest it lose all of its premium customers to Bouygues and Orange, leaving it only with value-based customers that are less attractive from a quad play strategy. Second, it needed to upgrade and expand its fixed line network to offer differentiated broadband service to its customers and bring them on-net. It announced aggressive plans on both fronts.

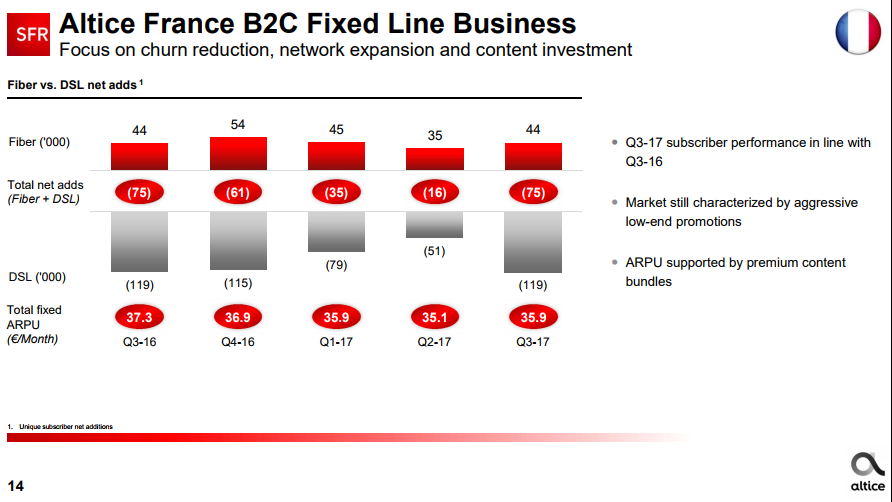

This slide from Q3 2016 provides a window into the state of churn (using B2B as an example) that Altice acquired when it closed the SFR acquisition near the end of 2015 and some of the early impact of its investments in 4G upgrades and pricing (reducing ARPU)

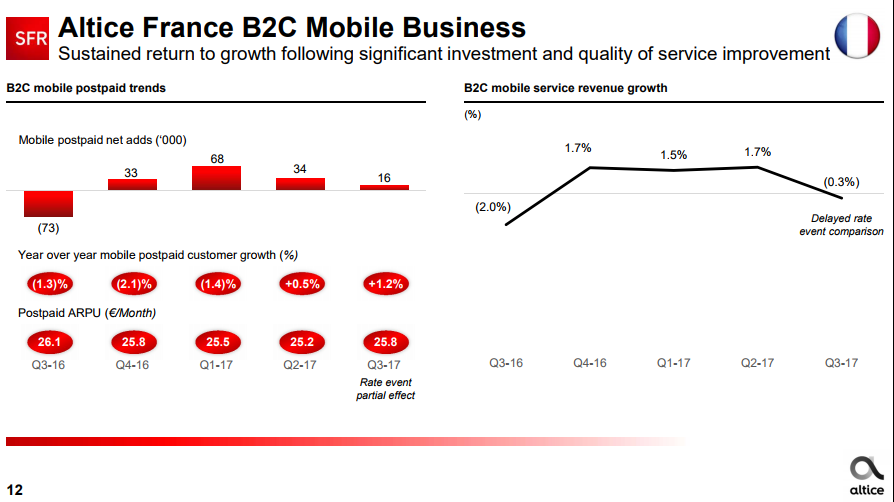

To Altice’s credit, on the 4G front, SFR is on plan, having caught up to Orange on 4G coverage and performance. This has allowed SFR to stabilize its B2C mobile subscriber base. Rolling forward to Q3 2017, you can see the stabilizing impact of Altice’s massive catch-up investments in 4G deployments on mobile subscriber net adds and ARPU.

On the fiber front, SFR is “on plan” from the standpoint of passing customers with fiber, but it is dramatically underperforming expectations on a net adds basis. SFR has mismanaged the customer experience, leading to high churn.

In theory, if you are an SFR DSL customer, when SFR passes your home with fiber, you should be able to have a low impact upgrade experience where - on the day of your choosing - a customer service rep shows up, installs your new fiber without tearing up your walls, sets up your CPE (customer premise equipment - modem, wifi, and set top boxes for TV (ideally in a single converged box)) and you leave happy.

In practice, disconnecting DSL was happening separately from connecting fiber, leaving some customers temporarily without broadband. The fiber connections were facing delays from CPE shortages and poor customer support and install experiences. Further, hyper-aggressive DSL promotions from Bouygues and Free (for as low as €1.99/month) were also driving churn from value-oriented DSL customers.

It is worth noting that it costs €8-9/month for any of SFR, Bouygues, or Free to rent a DSL line from Orange, so those promotional offers are money losing defensive responses by Bouygues and Free, who are well behind Orange and SFR in fiber deployments. They both worry that Orange and Altice are going to duopolize the fiber market and have decided it’s better to lose some money now with a goal of keeping that customer today and attempt to convert them to a higher value offer in the future.

Orange is deploying fiber at a similar cadence to SFR and, despite the competitive environment, is having much better commercial success than SFR. This implies that a great deal of SFR’s struggle is self-inflicted. SFR has poorly managed the customer experience as well as price increases related to increased content investment. This all has led to a very poor return on SFR’s fiber capital investment.

The following graphic summarizes the struggle. Note the deterioration in Q3 2017 – this is the proximate cause of the absolute slaughtering of Altice stock. What had been a gradually improving trend worsened and, worst of all, seemed to catch the company off guard.

From my standpoint, the DSL sub losses are frustrating, but the fiber net adds have been persistently terrible. Those should be 2x - 3x that runrate – 100,000+ fiber net adds per quarter. Some amount of DSL churn is actually desirable – we want to migrate DSL subs to fiber. Further, some slowness to the net fiber adds is understandable, because during the past two years, a big part of the fiber network investment has been to upgrade its existing cable network from HFC (hybrid fiber coaxial) to more pure fiber. In the case of an upgrade, Altice does not generate a fiber net add, but instead hopes to extend customer life. However, management acknowledges stubbornly high churn is the primary culprit - depressing a reasonably good gross adds number. Management states they are taking more than their natural share of gross adds. Given that fact, to end up with such low net adds implies extremely high churn – mid-20s vs mid-teens for the industry. To hit an upside scenario, this churn needs to be fixed.

Reason for Optimism in France?:

Whereas a year ago, for every four or five gross fiber passes, only one was a net pass, today SFR is nearly done overbuilding its own cable network with fiber. Fiber passes today are increasingly net new passes, with over 50% of gross passes in Q2 and Q3 being net new passes (400k gross passes per quarter of which >200k were net passes). That proportion should increase over time, as its existing footprint upgrade completes.

If we assumed 1.6 million net fiber passes per year, and SFR captures 25% market share (in line with its DSL market share), then it would add 400,000 net new fiber subs per year, which is more than double its current pace on the same capital investment. It is worth reiterating that – today – SFR and Orange are the only two players to have a meaningful fiber network in place. As a result, it is not hard to imagine taking share north of 25%, but that is for another day.

So why might SFR improve its penetration rates?

Armando Pereira and Management Focus:

Altice’s network guru is Drahi’s longtime partner Armando Pereira. He is considered expert in designing and building high performance network and operations processes. When Numericable acquired SFR, it shortly thereafter announced the acquisition Portugal Telecom, which would close six months after SFR. Pereira is Portuguese and left SFR after six months, dropping into PT to help lead its turnaround.

In PT, Pereira took a business declining 9% top line with 38% EBITDA margins and drove it to flat topline and high 40s EBITDA margins. While this was a great success, it meant he was not spending his time on Altice’s largest asset – SFR. Michel Combes, the successful former CEO of Alcatel, was brought in as “professional management” to run SFR. Simultaneously, Drahi and former Altice NV CEO Dexter Goei (who became Altice USA CEO) began spending time on the newly acquired US assets (which have performed exceedingly well since Altice took over). While key teammates worked on non-French assets, SFR was not going well and, in or around September 2017, Pereira quietly returned to France. Our understanding is that he began to uncover how poorly things were going at the raw operational level.

Management was overhauled after the Q3 earnings announcement. Combes retired and Drahi’s personal focus returned to Europe. Armando was officially tasked with focusing on improving the blocking and tackling of processes, IT, call center, customer technicians, and physical network infrastructure (the non-commercial elements - not content, pricing, packaging, marketing, etc.). Everything behind the scenes. Within Altice, he is considered exceptional at churn reduction through his ability to identify and correct root causes. We believe he will have (and likely already is having) a positive impact, but it will take several quarters to get SFR’s net adds to a more healthy place.

Altice PayTV – Valuable, Unique Content:

Unless you believe the French citizenry is suddenly going to stop watching its highest rated sports content - Champions League, UEFA, and EPL - we believe Altice owns a “hidden” asset in its content rights (particularly in relation to its implied Altice Europe stub market cap).

In a controversial move this past May, Altice announced it had acquired exclusive rights to European Champions League soccer for France and Portugal for three seasons: 2018-2021. It will pay €350 million per season for the right. That represents a doubling in the licensing cost from what Canal+ and beIN Sports had previously been paying (on a shared basis).

SFR had previously invested in acquiring exclusive rights to EPL (English Premier League – think Manchester United vs. Manchester City), Portuguese rugby, and many other sports. As a result, beginning this summer, if you want to watch the world’s best soccer and you live in France, you have to either become an SFR pay TV customer, pay Altice PayTV for its OTT sports package, or hope your pay TV provider (e.g., Orange) negotiates a wholesale deal with Altice PayTV to redistribute this to its customers. It is hard to come up with a perfect analogy, but it would be as if DirecTV acquired the rights to much of the NFL’s regular season and was the exclusive distributer of every playoff game… and the playoffs last off and on for most of the year. If you don’t have DirecTV or subscribe to DirecTV Now, you can’t watch.

The Champions League preliminary rounds will begin in mid-2018 and continue through June 2019. Altice PayTV’s exclusivity begins in August and continues through 2021’s championship game. Obviously, this is highly differentiated content. Under the new Altice PayTV structure, the intent is to maximize monetization either by driving new subs to SFR or by extracting rent from competitors’ subs.

SFR originally directly purchased the rights to this premium content, but given its poor subscriber net adds on the fixed side, Altice became increasingly concerned that SFR alone would under-monetize the high cost assets. As a result, in conjunction with the US spinoff, Altice announced the new Altice PayTV subsidiary. In essence, SFR granted APT the content rights and made a €300 million payment to APT to escape the content cost obligation (see schedule below). In exchange, SFR receives a below market content licensing deal back from Altice PayTV (SFR pays APT ~€50 million p.a. + certain revenue sharing).

As the content owner with its own P&L, APT will now attempt to extract full value from these rights by licensing them to other parties and bundling a consumer OTT offering.

We believe consensus attributes very little value to APT’s content driving either subscribers to SFR’s telco services or generating value by re-selling the content via other channels. Given the costs are already included in everyone’s go-forward Altice NV estimates, we believe incremental revenue could be very high contribution margin revenue. It is not hard to believe that this alone could generate nine figures of incremental margin. That would be quite substantial, particularly in relation to the small stub value of ATC stock.

DSL Wholesaling Costs:

SFR pays Orange >€800 million p.a. in wholesaling expenses for leasing lines and DSL to resell to SFR customers (under the SFR brand). Orange has this arrangement with all of its competitors in France and the cost is governed by regulation. A part of the SFR thesis has long been that a meaningful chunk of its fiber CapEx investment will be funded by the wholesaling savings. The execution on this has been poor, as rather than migrating to fiber, many have churned as a result of poor customer service or to even lower-priced competitive offerings.

All that said, this remains a large operating cost for SFR. It seems largely inevitable that it will be going down dramatically as SFR and Orange both drive the fiberization of the country.

Q3 Report:

Altice announced Q3 2017 earnings in early November and the bottom fell out of the stock. The aggressive response of Mr. Market seemed to catch management off guard; they seemed to realize they were reporting a somewhat weak quarter, but clearly did not expect the slaughtering that they received. Welcome to levered equity world.

For better or worse, the company seemed to take the market’s response seriously and subsequently announced a number of changes, which I’ve already discussed.

-

CEO Michel Combes resigned and a management reorganization was announced

-

Armando Pereira officially turned his focus to France

-

New, lower leverage targets in the US

-

Spinning off the US and all the associated movements (dividend, Altice PayTV, etc.)

-

A strategic review of assets with a view toward selectively selling to deleverage

In our view, Q3’s results were actually not that surprising. They were at the low end of guidance, with France worse (fixed churn) and the US continuing to perform well. Our view is that investors are responding to the extreme stock price move, but not calibrating the move in the context of Altice’s leverage and EV/EBITDA multiple from before Q3. With the consolidated group at 5.3x net debt/EBITDA and the stock trading at €16 (just prior to announcing earnings), the overall enterprise was trading at about 7.3x EV/EBITDA, implying an equity multiple of 2x. This means a one turn re-rating down in the EV/EBITDA was a 50% decline in the stock. That is what has happened. Further, because ATUS stock is down much less than Altice NV, the implied impact on the pro forma non-US stub has been even more dramatic.

Altice also has given guidance that Q4 French revenue would continue to struggle as certain low margin B2B and wholesale voice profits are challenged, while the core B2C business trends have been more stable.

If we zoom in on Altice NV post-spin (ex-USA), it has generated nearly €6 billion of EBITDA on an LTM basis. With €32.6 billion of gross debt and €2.5 billion pro forma market cap (of which €1.6 billion is cash and €0.3 billion is ATUS stock), it is trading at 5.1x net debt/EBITDA and 5.6x EV/EBITDA. This puts the equity stub at ~0.5x (net of cash). While nothing says the equity can’t fall 90% more, we believe the post-spin Altice NV stub has explosive upside. In a situation where it is simply valued at 7.0x EV/EBITDA, the implied equity could be a 3x. Note that Liberty Global (LBTYA) trades at 9.5x EV/LTM EBITDA6. In the meantime, the free cash flow yield is exceptional for the levered equity.

It is worth mentioning that given the reasonably strong operating KPIs that both Orange and Bouygues Telecom reported for Q4, it wouldn’t surprise us if SFR’s 4th quarter KPIs rhyme with Q3.

Summary:

Altice has upset its owners, disappointing them repeatedly in France. Its other acquisitions have gone reasonably well, with each of the US, Portugal, and the Dominican Republic as relevant examples of strong execution and value creation. Altice USA’s stock has been dragged down by association with its European brethren, despite strong fundamental performance and reason to believe large opportunity lies in front of it. Altice Europe’s implied post-spin equity is trading at heavily distressed multiples, despite its credit stack largely remaining at or near par. As a result, there is an opportunity for very large free cash flow yields and, if things simply don’t worsen, exceptional returns. If France actually improves, we believe the post-spin stub could provide abnormally high returns.

Footnotes:

1. Assumes Fx of 1.24 USD to euro. ATUS market cap of $14.7 billion = €11.8 billion. 70.5% of €11.8 billion is €8.33 billion. For Altice NV, assumes 1.205 billion shares (ex treasury shares). At €8.00 per share, Altice NV market cap is €9.64 billion. 8.33 / 9.64 = 86%. Adjusted down for the $1.5 billion dividend, Altice NV’s ownership of ATUS is worth €7.5 billion. 7.5 / 9.64 = 78%. Altice NV will retain 3.3% of Altice USA (~4.7% of its stake), making the distributed shares of Altice USA worth ~75% of the total purchase price of Altice NV today.

2. Altice owns 100% of each of the largest assets, such as SFR, Numericable, and Portugal Telecom, but owns less than 100% of certain assets, such as its French content subsidiary NextRadioTV, where that founder Alan Weill owns 49%.

3. Like Charter and Comcast, Altice USA does have a large public wifi network and recently signed an MVNO with Sprint.

4. In the Dominican Republic, Altice is just now fully “converging” its offers, after winning a long sought regulatory appeal.

5. As of 2/15/18: EV/NTM EBITDA, Charter at 10.1x, CableOne at 10.5x, Comcast at 8.4x.

6. As of 2/21/18.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Free cash flow generation

- Deleveraging divestments at attractive multiples

- US spinoff

- Stabilization in France (or simply not becoming dramatically worse)

| show sort by |