| 2016 | 2017 | ||||||

| Price: | 16.72 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 36 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 593 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 599 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,224 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Pair trade

- REIT

Description

Long SBY Short AMH

Overview

Silver Bay (SBY) and American Homes 4 Rent (AMH) are internally-managed REITs focused on acquiring, leasing and operating single-family homes as rental properties (known as SFR companies). We propose a pair trade going long SBY, a better operated, cheaper-valued company with a significant prospect of being a take-over target while shorting AMH, which trades at an undeserved premium to its peers despite likely idiosyncratic headwinds. Additionally, this trade benefits from positive carry due to the higher dividend yield of SBY vs. AMH.

Background

o The single family home category is extremely fragmented, with an estimated 14.2M single family rental homes in the US (representing 1/3rd of the overall rental market and ~20% of total Single Family homes overall) with institutional investors owning only a small percentage of this sub-market.

o Publicly traded REITs own less than 100K homes combined.

o Following the real estate crash during the recent recession, a number of opportunistic, institutional buyers purchased homes by the thousand, and sought to create a new niche REIT category

o The largest homeowner is private company Invitation Homes, owned by Blackstone, with ~48K homes

o AMH is the largest of the public comps, which also includes Colony Starwood (SFR) and Silver Bay, owning 48K houses in 22 markets following its recent purchase of American Residential Properties (ARPI)

o AMH’s largest Metro markets include Dallas (9.4%), Atlanta (8.3%), Houston (6.8%) and Indianapolis (6.3%)

o By state, AMH is concentrated in TX (~20%), FL (~11%), GA (9%), NC (7.5%) and IN (~7%).

Comparison

o LONG:

o SBY is an excellent, focused operator with consistent results and margins

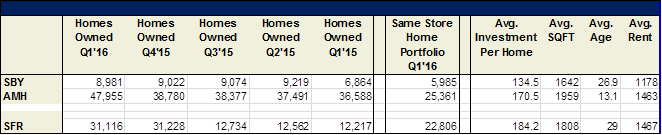

o Silver Bay Realty Trust owns ~9K homes

o Previously the company had been externally managed by a joint venture between Provident Real Estate Advisors LLC and an affiliate of Pine River Capital Management L.P.

o SBY internalized its management in April 2015 along with its acquisition of American Home Real Estate Investment Trust, which added ~2.5k properties to its portfolio.

o What its portfolio lacks in scale it makes up for in concentration with over 55% of portfolio in its top 3 metro areas and 70% concentrated in just 3 states.

o Top Metro areas are ATL (~30% of total), Phoenix (15%), Tampa (12%), Charlotte (~7.7%) and Dallas (5.6%)

o By State SBY is over 70% concentrated in 3 states, with GA representing ~30% of SBY’s portfolio, followed by FL (26%) and AZ (15%)

o This concentration has allowed the company to internalize certain service operations and self-manage ~95% of its properties directly in its top markets.

o Something which only the larger SF REIT peers have been able to pursue

o Given its focus on operations rather than building scale, SBY has also performed better and demonstrated a greater willingness to return cash to shareholders

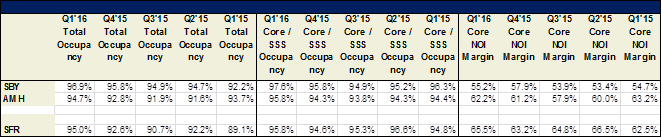

o SBY has led AMH in terms of total occupancy over almost all of the past 3 years, achieving ~95% or greater occupancy for the past 4 quarters.

o In Q1’16 SBY achieved rental increases of 4.8% on new move-ins and 3.3% on renewals, and Mgmt expressed that they are comfortable in achieving their target rent growth of 3.0 – 3.5% in 2016

§ Slightly lower than peers, due in part to SBY’s lower overall average rent price of ~$1,178 vs. ~1,450 for AMH & SFR, and because SBY is likely trying to maximize occupancy

o Mgmt hopes to continue to improve its turnover time from ~54 days down to ~40, noting it achieved ~44 days in March.

o Mgmt touts its hedge fund roots in focusing on an “absolute return basis” (cash-flow yield + home price appreciation)

o Ownership

o Irvin Kessler, an early investor in Pine River, owns 8.5% of Shares O/S

o History – Hedge fund Pine River created Two Harbors Mortgage REIT and acted as the manager, and after a few years, they decided to buy single family homes. Then along with Provident as a partner, they formed Silver Bay, which they later essentially spun out into what it is now. Pine River has since divested its stake in SBY

o Mgmt - Silver Bay CEO David Miller resigned in January for unclear reasons

o At the time of Miller’s resignation, lead independent director Thomas Brock was made Interim CEO while the company commenced a search for a permanent CEO with a strong real estate background

o Last week, Silver Bay named Brock permanent CEO

§ The fact that 69-year old Brock, a strong finance executive but not a real estate operator, was made CEO suggests to us that he is more likely to play the role of short term care-taker rather than seek to significantly expand the business

o Our expectation is that Brock will run Silver Bay efficiently until one of its larger peers (e.g. AMH, SFR or potentially Invitation Homes) finish digesting their recent acquisitions and make an attractive buy-out offer

o SHORT:

o AMH trades at an undeserved premium to its public competitors

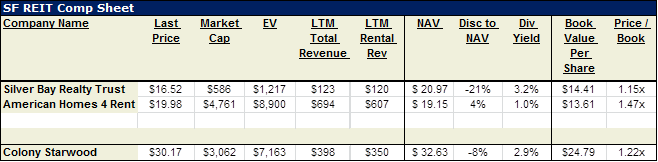

o Relative to NAV, AMH currently trades at a ~4% premium vs. a 21% discount for SBY (and a 8% discount for SFR)

o Price to book AMH is ~1.47x vs. 1.15 for SBY (and 1.22x for SFR)

o On P/FFO basis, AMH trades at over 20.5x ’16 FFO, while SBY trades at a similar level and SFR closer to 18.5x

o In terms of geographic markets and cap rates, according to Zillow data, AMH has ~5.9% weighted cap rate vs. 5.6% for SFR and 5.5% for SBY

§ The Street’s estimated NAV for AMH is ~$19/ share implying a cap rate of ~5.4%

o AMH rent growth has lagged the past two Qs, with 4.1% in Q1 on renewals vs. SFR at 4.8%, and SBY at 3.3%

§ In Q4’15, AMH renewals had 3.7% rental growth vs. 4.9% for SFR.

§ AMH exposure to Texas (20%) may provide some headwinds in the short-term both in terms of rent growth and tenant credit quality

o SBY maintains industry leading margins despite lacking scale, and most importantly pays out a higher dividend yield than AMH (as does SFR)

o AMH currently yields 1.0% compared to SBY’s 3.2% and 2.9% for SFR

§ AMH mgmt. has made no comments about prioritizing the increase of its dividend, despite its modest debt levels relative to its peers.

· In Q1, leverage is ~43% for AMH, vs. 52% for SBY and ~59% for SFR (net of NPL liquidation)

§ Growing the dividend would likely attract new investors, rather than repurchases which shrink the market cap and discourage institutional investors

§ On the contrary, SFR has promised increasing dividends w/ payout ratios closer to apartment REITs and SBY appears to be of similar mindset

o AMH’s NOI margin has been inconsistent, despite having the most scale

§ The impact is most notable in Q3 when seasonal factors such as summer moving and re-leasing activity weigh on occupancy and increases expenses

§ This is driven in large part by AMH’s lower retention rate vs. its peers.

· AMH’s retention rate has also been lackluster, ranging from the high 60s to low 70s over the last 3 years vs. Mid 70s to low 80s for SBY and SFR

o Ownership is concentrated in the hands of founders (8.5% of Shares O/S) and the Alaskan State Wealth fund (~19% of shares O/S)

Catalysts

o M&A – Given the recent takeout of ARPI by AMH and merger of Colony and Starwood, consolidation is a clear trend in the sector

o Very likely that SBY will be taken over as the larger players look to accumulate greater scale

§ While SBY is operationally focused, this is a business that benefits from scale (which currently seems to cap SBY’s NOI margins, given SBY is now four quarters past its last major acquisition

o This will likely occur at a premium to current share prices assuming the acquirer utilizes an all stock deal based on NAV

§ ARPI sale done at 17% premium to book and ~20% discount to Cons. NAV

§ SWAY/Colony deal a merger of equals with pro-rata ownership based on relative NAV weights

o Given a conservative estimate of ~$20mm of synergies available (e.g. no SBY G&A, minimal maintenance scale efficiencies), AMH could afford to pay a 15 – 20% premium and still purchase Silver Bay stock at 13 - 15x 2017 Pro Forma FFO/sh while its own stock trades at ~19x ’17 FFO

§ Even with such a take-over premium, a buyer would still be purchasing SBY at a discount to NAV

o Notably SBY’s footprint is closely aligned with the other larger SF REITS as AMH and SFR as both have sizeable presences in GA, FL, AZ and Texas.

o It seems that AMH has slightly more overlap relative than SFR, given it has exposure to smaller markets like NC and OH, while SFR has presence in CA, which AMH does not

§ However, the best outcome could be a sale to AMH with a divestment of California to SFR

o Improved margins

o As SBY laps its relatively large acquisition last year and begins to reap benefits of efficiency initiatives and higher retention rates, margins should improve

o Macro & Housing Market Trends - with the tailwind of near double digit rental increases likely in the rearview mirror[1], SF REITs must now focus on execution in terms of occupancy and cost controls, an area it has yet to prove itself in.

o Texas exposure of ~20% for AMH is particularly troubling given commodity downturn and likelihood for lower rents and higher delinquency rates in this area

o New supply presents itself as a threat to SF REITs, as multifamily construction rates are increasing posing a competitive threat to lower end homes, and single family inventory may finally start to grow again (currently, April’s single-family housing starts were at a seasonally adjusted annual rate of 778,000 units, down from a more than five-decade average of about 1.03 million, according to Census data. Meanwhile homes under $200K made up 19% of US sales last year down from 38% four years earlier)

o Lending standards continue to be loosened for lower-end/first time buyers causing the homeownership rate to tick up from its four decade low of 63.5% in Q1.

§ Currently lending standards are tight for those in the below 660 FICO score range, meanwhile AMH’s average tenant is ~650

o Operation hiccups - Although on a high level the business model is quite simple, given the unique attributes of single family homes, combined with seasonal, legal and other nuisances, the sector presents itself with a number of pitfalls and other difficulties that can hamper portfolio standardization, the creation of efficiencies, and profit margins.

o This is particularly true for AMH after its recent ARPI acquisition and its current shift from a prior focus on growth and getting occupancy into to the mid-90s, toward a focus on maximizing operating margins

o Unlike its smaller competitor SBY, ARPI was a mess[2], and while in terms of geographic overlap the deal made sense, AMH will likely have to spend significant time and resources cleaning up this portfolio in order for margins to progress toward that of legacy AMH.

§ These large scale changes will take time to integrate given the dynamics of leases and ability to renovate, etc., AMH noted it expects a 24-month period to renovate legacy ARPI homes to AMH standards as they turn.

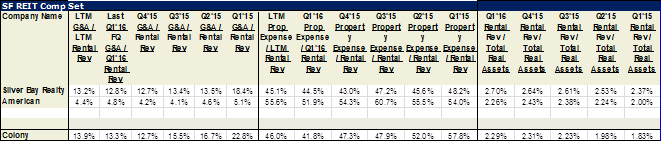

§ AMH already generates the highest proportion of its total income from tenant chargebacks and fees relative to its two peers.

· AMH generated over ~10% of its total revenue from chargebacks in Q1, vs. ~4.5% and 2.3% for SFR and SBY respectively.

· Exact cause of this is unclear but it reflects poorly on AMH’s current tenant screening processes and does not seem sustainable longer term

o Interest Rate Hikes are threat to all REITs but their exact impact on this subsector is unclear, given impact on homeownership trends

o A pair trade minimizes exposure to this risk, not to mention recent macro events (i.e. Brexit) have made this a smaller likelihood in the near term

o AMH faces near-term competition for largest in sector title

o Inevitable IPO of BX’s Invitation Homes likely to lead to re-allocation of sector capital to largest, perceived better operator

Risks

o SF REITs begin to trade in-line with the multifamily apartment sector, which trades at a higher FFO multiple (~1-2 turn premium on average)

o The risk is mitigated by the hedged long/short trade

§ Note – while we like SFR, the stock has recently recovered from its prior larger discount to AMH, and it lacks the M&A target optionality of SBY

o HPA weakens in SBY core markets thereby weighing on its NAV vs. AMH

o Consolidation story never plays out

o Geographic concentration particularly in South-East leaves SBY vulnerable to storms or regional trends in rental markets (top 3 states are also relatively easy for new supply to be built)

o However, recent data suggests that lower housing remains underbuilt, albeit over the past few years multifamily construction has surpassed nearly all the averages set the prior decade.[3]

o Relatively older homes for SBY; could lead to more capex

o AMH relents and ultimately decides to raise its dividend more in-line with peers

o Volatile/drop in the overall market may lead to temporary AMH outperformance due to perception of higher quality

Comp Tables

[1] In April, Apartment rents began to slow as Axiometrics’ April data for the top 20 apartment markets showed revenues per available unit (RevPAU) up +4.4% Y/Y, driven by +4.4% effective rent growth Y/Y, while occupancy dipped -4bps. April’s effective rent growth Y/Y moderated from March’s (+4.7%) and +4.8% increase in February. RevPAU growth Y/Y in April of +4.4% is lower compared to March’s +4.7% and +4.8% in February and a clear deceleration from April 2015’s +6.4%. Other forward indicators include hotel room revPar, which has also shown reliability in being a forward indicator of rental revenue growth for apartments, and has been on the down trend over recent Qs. Data trends from the SF REITs themselves is somewhat less reliable given the narrow field of players, recent consolidation and relatively short history, which has been mostly dominated by a focus on maximizing occupancy rather than rental rate increases.

[2] On its Q1 call, AMH noted that of the ~9K homes acquired from ARPI, ~1.3K do not conform to AMH quality standards and will likely be sold. Also noted that ARPI’s bad debt was higher, but that AMH has resolved almost all of the delinquencies

[3] The US Census Bureau data for 2015 shows 657k 1-4 family units and 310k 5+ multifamily units were completed, in addition to 75k government subsidized affordable units and 64k manufactured housing units. Taking into account 333k units taken offline due to obsolescence, net new units of 774k met approximately 1.1 million of newly formed households. This imbalance should lead to further home price appreciation for single family and rent increases for multi-family

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Listed above

| show sort by |